Blog

Faster Than We Can Learn: The Need for Digital Tech-Enabled Underwriting

Let’s talk about jellyfish risk for a moment. I saw lots of them on vacation this year at Gulf Shores, Alabama every day!

In a world filled with risks of all kinds, shapes and sizes, the jellyfish is a little difficult to pin down. To some, the risk might seem insignificant, invisible, or shapeless — kind of like the jellyfish itself. We don’t see them easily, so they fly under the radar. There is no frightening dorsal fin sticking out of the water.

Yet the risk that jellyfish pose is real and growing. Approximately 150 million people are stung each year by jellyfish and hundreds are killed.[i] In fact, you might be surprised to know that more people die each year from jellyfish stings than from shark attacks. In the Philippines alone, 20-40 people die from jellyfish stings each year.[ii] And no … I was not stung by one!

“Well, that’s a life insurance statistic,” you might think.

Jellyfish, however, spread the risk around. P&C insurers might be interested to know that jellyfish can damage personal watercraft. They can disrupt water-based businesses. Annually, they shut down 2-3 power stations by clogging water filtration systems. They have caused near meltdowns at nuclear power plants.[iii]

Higher overall ocean temperatures likely from climate change are causing jellyfish to roam further afield from their common habitats. The growth of new breeding areas, such as offshore wind turbines, oil rigs, and oyster beds, has allowed jellyfish to gain a foothold in more northern tidal regions. In short, jellyfish are thriving, and jellyfish risk is a real thing.

Are insurance underwriters keeping track of global jellyfish trends?

The world of risk is changing faster than we can learn.

It may still seem trite to us, but the jellyfish makes a great example of risks that exist and are growing, but no one is tracking because no one, except marine biologists, really has the time to track jellyfish or the risk implications. Every risk, however, is trending in some direction. Risks are growing. Risks are combining. Risks are shrinking. Some risks are staying the same. How can we see what we don’t recognize as a risk until it sneaks up on us too late? What other risks are changing due to climate change we are unaware of? How can we predict what might happen with that risk in the future?

Like it or not, the world is changing faster than we can learn about new risks and risk trends. At the same time, we have technologies capable of tracking nearly any risk with data, improved methodologies, and AI/ML. In Majesco’s recent thought leadership report, Underwriting and Loss Prevention to Tackle Rising Insurance Costs, we take a look at some of these changes in risk and take a closer look at the technologies that should be employed to manage risk and lower costs for insurers to become adept at learning just as fast as the world is changing. In today’s blog, we consider timing. Should insurers be trying to tackle today’s underlying risks, or could they begin to gather what Majesco would term, “tomorrow’s insights today?”

Is the unpredictable actually predictable?

Today, we are now seeing increasing environmental, societal, and technology risks that have the potential to intersect and significantly disrupt people and businesses. The Marsh Global Risks Report 2021 for businesses notes that the economic, technological, and reputational pressures of the present moment risk a disorderly shakeout, threatening to create a large cohort of workers and companies that are left behind in the markets of the future.

For example, increased extreme weather events and natural disasters have an unprecedented and increasingly significant impact. According to the National Oceanic and Atmospheric Administration, the United States experienced 20 separate unique billion-dollar weather and climate disasters in 2021, placing it second to 2020 in terms of the number of disasters, 20 versus 22, and third in total costs of $145 billion, only behind 2017 and 2005.[iv] Forest fires seem to be increasing, and with them, property loss. Recent tornado damage has increased, and the traditional tornado avenues seem to be expanding.

In a converging trend, construction costs are rising due to supply chain issues, increased costs for materials due to inflation, and a lack of construction workers. The rapid rise in home prices and high demand has left many properties uninspected (buyers agree to forego inspection as a “perk” for sellers). A family member did and within weeks we had to replace not only the furnace and air conditioner but also the electrical panel that was recalled years ago due to fire hazard – a significant unknown risk. The result is likely unidentified risks and underinsured properties for both the insurer and the insured – creating significant risk gaps that have financial, customer experience and reputational implications. Loss prevention strategies must change if insurers wish to remain stable and growing.

Insurers must adapt. The only way the unknown risks become a part of business strategy is if underwriting accounts for changes that are in constant motion, using variables as diverse as climate change and construction prices. In many ways, both of these elements are predictable. Climate change is certainly headed in a particular direction while labor and construction costs have actually been rising fairly consistently for over a decade, with a larger bump in the past year. (See the Mortensen Construction Cost index here.) Even though the risk may appear to be growing faster than we can learn, the reality is that we may simply need to use technology to teach us faster.

Limiting the element of financial surprise

Whether or not insurers can learn about risk fast enough, a lack of effective pricing adaptation will come back to bite them with high loss ratios and unprofitable books of business. Insurers don’t need to control the uncontrollable world. They need to understand it in ways that help them adapt pricing before financial results cause unwanted surprises. Granular detail is no longer about “getting in the weeds.” It is about preventing the loss that comes from a lack of risk knowledge and pricing application.

Operationally this requires a combination of digital business solutions including next-generation core, digital loss control, digital underwriting workbench, AI/ML models, and the ability to ingest a range of data sources from customers, including unstructured, video, geospatial, social, IoT devices, and more, to create real-time risk management and insights.

Insurers are increasingly focusing their time and resources on how they can better assess risk and prevent losses to improve underwriting profitability and customer experiences.

Insurance has always been a data-driven business, but access to new data sources with AI/ML is redefining the industry. Today’s increased catastrophes, market environment, and pressure on profitability demand a greater focus on preventable losses and better outcomes through underwriting profitability, proactive risk mitigation to minimize or eliminate claims, and enhanced customer experiences.

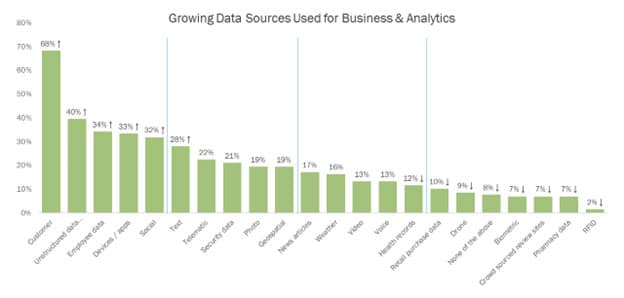

Majesco’s 2022 Strategic Priorities research indicates that insurers are increasingly investing in intelligent digital underwriting, loss control, and AI/ML solutions.[v] Insurers are expanding the data sources from customer data to unstructured data such as loss runs and loss control reports to new digital data sources from devices, video, geospatial and more, as represented in Figure 1 below. All of these efforts hold one thing in common: the reduction of financial surprise through efforts through faster learning.

Figure 1: Data sources used for Business & Analytics

The new and greatly improved role of data — teacher, tutor, and communicator

An increased focus on loss control and other data has resulted in increased volume, variety, and velocity of structured and unstructured data sources. Loss control has moved from surveys with questions, checklists, and photos; to leveraging real-time data from smart devices, video, images of labels, and more through risk engineering firms, customer self-surveys, and video-guided surveys.

Insurers can use the richer data loss control and other data ingested with advanced AI/ML for improved risk assessment, appetite analysis, underwriting, and pricing. Advanced AI/ML enables insurers to analyze data in real-time to drive intelligent decision-making. By identifying hazards and providing recommendations as data is ingested or collected, carriers and vendors can now create more value by proactively addressing issues and providing recommendations in real time.

This significantly broadens the role of underwriting and loss control in an organization. Suddenly, instead of just pricing with greater clarity, new data and analytics along with loss control can educate insurers on how to best respond to risk trends. When paired with the new tools of digital customer service, we can help train insureds on how to avoid risks, then communicate the impending risks as quickly as they are recognized. It shortens the time period between data capture, predictive analytics, and timely communication.

Letting the past teach the future using cutting-edge technology

We may not have an accurate picture of what jellyfish will do next year, but we do have a fairly accurate understanding of the damage they have done recently and in the past. In this way, a better grasp of the real impact can be ascertained with some degree of certainty. The past can be effectively applied to the future.

Insurance loss control technologies, such as those offered by Majesco, have this methodology in mind.

As quickly as the future is changing, insurers still understand the results of damaging and catastrophic impacts. When it comes to structures and property, they can get a fairly accurate picture of which properties are at risk.

In Majesco’s recent blog, “Is it Time to Hire New Data?,” Patrick Davis explains how Majesco clients can now access loss control data from 16 million property surveys, including 200 million photos. When insurers plug new photos into loss control software, machine learning takes over and analyzes the risks within an electrical panel, a hot water tank, a roof, a backyard, etc.

Risk characteristics contained within the database allow Majesco to create models that can determine how much risk there is for almost any specific given property. It is an excellent example of how technology can help insurers cope with a world that is changing faster than we can learn.

Your next step now

Insurers have been excellent risk product providers for a very long time. But as the future seems to come faster and unpredictable risks like jellyfish seem to pop out of nowhere, insurers need to get ahead of the future in any way they can. They need technologies that can work holistically to ingest high volumes of data, analyze disparate types of data, learn what is up ahead, and communicate it both internally and to policyholders.

The “next generation” of underwriting uses today’s technology in ways that will help insurers understand and manage the future of risk before it happens.

To read more about loss control, be sure to download Underwriting and Loss Prevention to Tackle Rising Insurance Costs. Contained in the report is a short case study on how the described technologies have helped a commercial property carrier to improve profits with better data and fewer travel and staffing hours.

And remember … watch out for the jellyfish!

To learn more about Majesco’s Underwriting 360, Loss Control, Data & Analytics, and P&C Core Suite solutions, visit the Majesco website today.

[i] Chabin, Michael, How to handle the worldwide jellyfish threat, The Washington Post, July 5, 2019

[ii] Law, Yau-Hua, Jellyfish almost killed this scientist. Now, she wants to save others from their fatal venom, Science.org, November 8, 2018

[iii] Izadi, Elahe, How jellyfish have become nature’s ultimate guerrilla protesters against power plants, The Washington Post, July 7, 2015

[iv] Smith, Adam, “2021 U.S. billion-dollar weather and climate disasters in historical context,” NOAA Climate.gov, January 24, 2022, https://www.climate.gov/news-features/blogs/beyond-data/2021-us-billion-dollar-weather-and-climatedisasters-historical

[v] Majesco, “2022 Strategic Priorities Report”