Blog

Unlocking MGA Growth Momentum: Insights and Priorities to Compete and Thrive

For Leonardo da Vinci, art and science were not separate spheres. Excellence in art and science was a matter of observation and application of the physical principles of nature and life. DaVinci’s observations led him to unlock many truths about how the physical world operates. These observations gave him ideas for how people could derive utility from understanding. The new knowledge could transform real-world attributes into functional tools and machines to conquer real-world issues.

To uncover the world’s mysteries, Da Vinci placed himself in locations where he could observe, record and consider the meaning of what he found. Did it have a practical use? In a way, this is the same methodology used by today’s MGAs and the insurers that value MGA ingenuity. MGAs are in the right space at the right time to observe and act.

Most insurance companies can’t be everywhere at once. They can’t observe every segment in the industry. They aren’t always privy to where there is value and risk, or where new technologies might be applied.

MGAs, however, live it, breathe it, understand it, grow in knowledge of the new risks, and they see the application of insurance and the value that it can bring to underserved markets. This is what gets many of them off the ground — if they can create a profit formula.

Opportunities for MGAs, Insurers and Partners

MGA growth is unprecedented. There are now estimated to be more than 1,000 MGAs in the US, and as a group, they have experienced double-digit premium growth in the last four consecutive years. Majesco is at the forefront of MGA technology innovations, helping to facilitate that growth by modernizing MGA and insurer platforms so that they can reach new markets. In our recent thought-leadership report based on primary research with MGAs, MGAs’ Strong Growth and Growing Role in the Insurance Market: Strategic Priorities 2025, we compared MGAs and Insurers and we looked at MGA strategic priorities year-over-year.

I asked David Gritz, Co-Founder and Managing Director at InsurTech NY to join me, Denise Garth, Chief Strategy Officer at Majesco, in a webinar discussion and analysis of the research. David’s unique place in our industry allows him to get an excellent view into MGA motivations, operations and technology trends.

Together we covered:

- The State of the MGA market

- Operational Priorities for MGAs vs. Insurers

- Technology Foundation: MGAs vs. Insurers

- Implications and Recommendations based on findings and experience

Today’s blog contains abridged highlights from our discussion. For the full presentation, be sure to view Unlocking MGA Growth Momentum: New Insights and Priorities to Compete.

The State of the MGA Market

Denise Garth

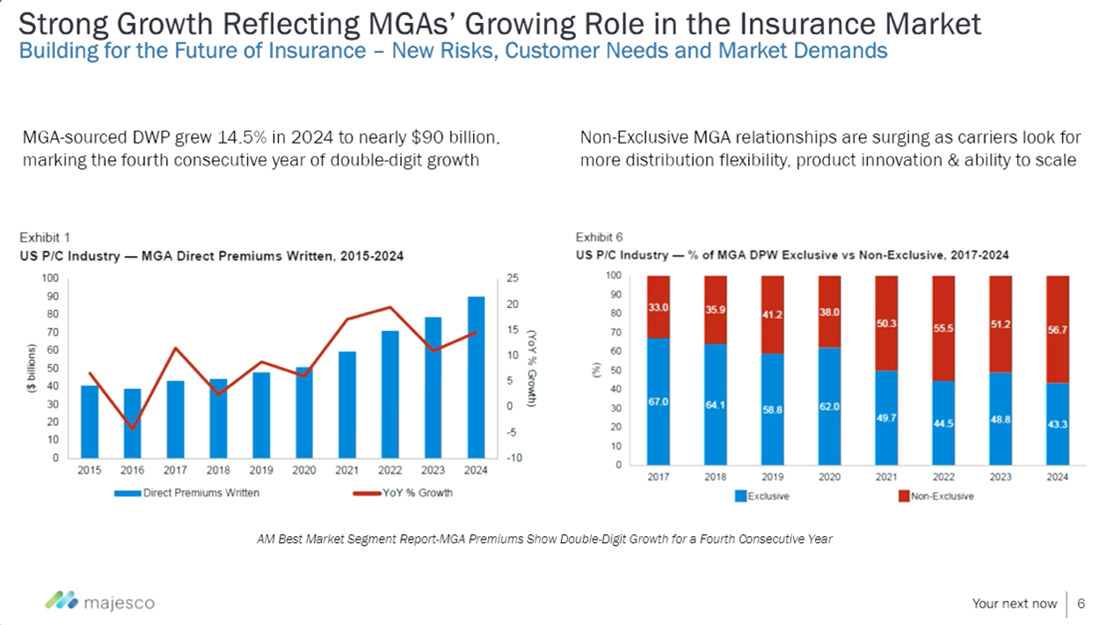

MGAs continue to have a growing role in the insurance market because, in many cases, they are unhindered in their ability to look at new, different risks and be able to assess those risks and underwrite those risks and bring products to market. Direct Written Premiums for MGAs grew by almost 15% in 2024. It is interesting that non-exclusive relationships with insurers are also growing. More MGAs are choosing to work with multiple insurers, rather than exclusively with only one insurer.

Figure 1: MGAs’ Increasing Role

David Gritz

Typically, how it works with most of the startup MGA’s we work with is they will start with one insurance partner that will act as the front and the reinsurer. As they become more mature in years three through five, they will start to diversify. The next step may be to set up a reinsurance panel, and then eventually they will have multiple insurance partners across multiple products.

Denise Garth

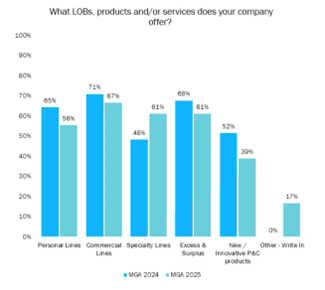

When we asked the MGA’s that we surveyed where they are focusing as it relates to lines of business and risks, the responses are fairly similar to last year. Specialty lines have really grown in focus in the last year, which in many cases could also represent some different types of products that they are bringing to market.

Figure 2: The focus of MGAs

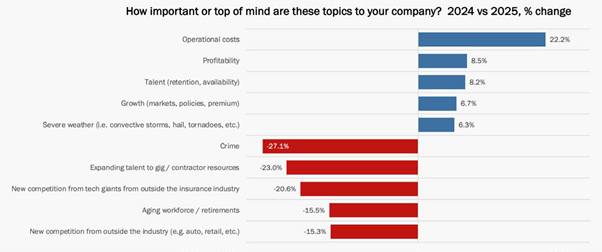

We also asked MGAs what was top of mind for them as they think about their business and the market. The top five areas were: operational cost, profitability, talent, growth, and severe weather.

Figure 3: Year-over-year changes in MGAs’ top of mind issues

This intensification of operational cost we see is mirrored on the insurance side as well. MGA and insurer operational expenses are continuing to rise.

David Gritz

We are definitely seeing alignment between operational costs and their impact. For example, in the past, VCs used to say to startup MGAs, “Here’s $5,000,000. Figure out what to do with it.” Now investors are more savvy. They know how much the core infrastructure should cost and they’re not going to let the founders go out and build it. They want them to buy something existing.

One area in that MGA startups may differ from the established MGAs answering this question is that there is a tremendous amount of pressure on startup MGAs for growth. For them, growth may be the #1 top of mind topic.

Denise Garth

At Majesco we looked at MGA’s growth and looked at key areas within their strategic initiatives. We saw some differences from last year, but also differences from insurers’ activities.

Insurers are more focused on replacing core insurance systems. MGAs have had a decline in this area.

MGAs are accelerating the use of different operating models to bring new products to market, reaching different channels. This is good for the market overall, particularly for those insurers that are working with MGAs. Having modern next-generation technology makes it much easier to establish connections between the MGAs and insurers.

David Gritz

I totally agree with you. MGAs, compared to the insurers, have a bigger focus on growth and have been experiencing more growth.

When it comes to changing core systems, for startup MGAs, we find that it is a big lift for such a small team, so they sometimes make their choice and then they are stuck with it for the next five years. It’s really difficult for them to make a change. We do know a couple that are doing it.

With the carriers, they essentially see changing their core as almost like a burning platform. They see that the MGAs are much more nimble than they are because they’re not beholden to their old COBAL systems. MGAs can launch products faster. MGAs can adjust to new channels faster. So, carriers feel like if they don’t do it now, they’re really going to fall behind.

Denise Garth

People are also considering whether their solutions will allow them to leverage data and analytics, particularly around AI. Having access to that data is bread and butter for MGAs. Being able to assess data trends from a risk and an underwriting perspective will help them as they bring products to market.

Operational Priorities

Denise Garth

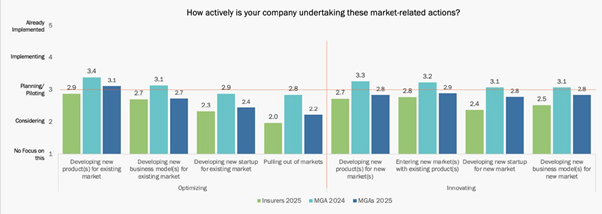

Let’s begin with market growth initiatives. MGA’s are really leveraging and strengthening their competitive levers around developing new products for existing markets and new markets.

Figure 4: Market-related actions: MGAs vs. Insurers

Increasingly, MGAs are looking at newer technology to be able to test, grow and scale effectively as opportunities arise from the changing risk environment.

David Gritz

So with many of these MGAs, it is either grow or die. If they don’t get to $10 million in premium in a short period of time, they’re just not going to exist anymore. Their fronts are not going to support them. So that’s absolutely a focus for them.

But there are some startups and newer MGAs — ones that are in their first three to five years of business and they might have mastered an area — that are looking to share resources with other MGAs, whether it’s a reinsurance panel or it’s some of the software that they have built — they can sort of act as a super MGA program together.

I think that this is going to become more common. For these programs that are anywhere between $10-$100 million in premium, it is well worth it for them to find an incremental partner that’s going to bring them an additional $10 million premium.

Distribution

Denise Garth

So, let’s talk about affinity relationships for a moment. Affinity partnerships are increasing on the MGA side. Most of us associate affinity-related marketing and affinity relationships primarily with insurers.

It is interesting, however, to see how MGA’s are getting into this. They are seeing it as a way to bring in different kinds of products and to be more nimble. And in their case, it may not be the big affinity relationships, but they can target some of the smaller affinity groups and communities.

David Gritz

I concur with you on the affinity side. We have a portfolio company that’s in the home warranty space. Their main channel is selling through realtor’s closing companies and mortgage companies. Those types of non-insurance affinity relationships are natural for home warranty insurance products.

We also have a portfolio company that offers an extended warranty for goods sold online. They have found that there are private-equity-owned groups that have multiple retail or e-commerce companies. So if they can affiliate with the parent, then they can start to develop relationships in different slots.

If companies are creative, they can find these niche channels. They should never stop fostering their broker channel, but sometimes there are alternative ways to gain access to a whole group of customers through one relationship.

Denise Garth

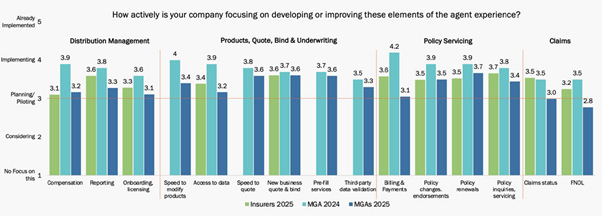

Let’s backtrack for a moment to talk about those brokers and agents. The Majesco report looked at how MGAs are developing and improving theagent experience.

If you look at the graph, MGAs and insurers are very similar in areas like compensation, reporting and onboarding. In most ways, both MGAs and insurers want to be easy to do business with in order to get business through the agents.

Figure 5: Agent experience: MGAs vs. Insurers

One thing that I would highlight here is access to data and the speed to modify products, in particular the access to data. For both insurers and MGAs, it’s all about ease of doing business, quick onboarding and being able to give agents the quotes that they need in a quick time frame.

David Gritz

It depends upon the lines of business, but speed to quote is how some of these MGA’s can win customers. They have to demonstrate they have better service. Do they have an easier broker portal to use? Have they created a submission process that doesn’t require a heavy lift? That’s what’s going to win the agents to actually send them submissions.

For some lines of business that are higher frequency, like a warranty business where policies are very small, it has to be a seamless transaction that’s embedded into whatever you’re doing.

The other thing that we’ve been noticing is that when startups get started, they’re all about growth. But once they’re in years two through five, they have to think about how they maintain as many clients as possible. Are they keeping track of who is purchasing, and through which channels, and if they are renewing?

Probably half of the MGAs that we see could get better and grow faster if they just cut the churn and improve their existing relationships by improving their CRM.

MGAs lag behind insurers in AI Chatbots

Denise Garth

MGAs are lagging behind carriers when it comes to AI Chatbot use. It could just be a reflection on the types of technology being used, or the maturity and the size of the MGA. But, AI Chatbots are an area that both insurers and MGA’s are going to have to get serious about.

David Gritz

So I would actually make a small distinction on the chatbots to reinforce their potential. There are customer-facing chatbots and there are channel-facing chatbots. From what we’ve seen on the insurer side, there is a lot more appetite to set up chatbots that your brokers can work with because they need to have a usable knowledge repository. They need to be able to get questions answered about how you look at underwriting.

Most carriers have this in static PDFs that are not very easily accessed. Establishing AI chatbots will cut down on support time and keep underwriters more productive.

Technology Foundation: MGAs vs. Insurers

Denise Garth

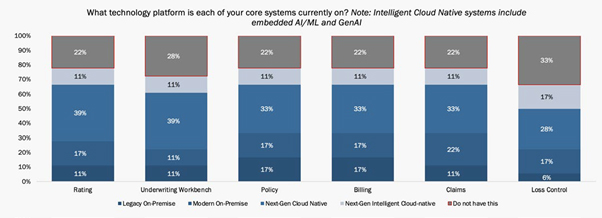

Only about 45% of the MGA’s have cloud native or modern next-gen core systems with a lot of legacy. Those that probably don’t even have a core system may be using spreadsheets; they may be using agency management systems, etc.

Figure 6: MGAs’ core and operational systems technology platforms

If they’re going to be in a growth mode and they may be moving into a larger organization that is handling a broader set of products and reaching different types of markets, then having the right technology foundation is going to become increasingly important.

Private equity firms have been buying a number of MGA’s to be able to consolidate them and drive some operational efficiencies. Many of the private equity groups, when they’re looking at the potential acquisition of an MGA, look at which technologies they are using. If they can drive operational efficiencies and they can handle more volume, it can make the MGA much more profitable.

Insurers Outpace MGAs in Overall Data and Analytics Capabilities

Denise Garth

Many MGAs have their own models for underwriting because it’s really around the unique risk that they cover. But I do think it’s interesting that we still have a number of MGA’s that are experimenting with the full spectrum of AI technologies or capabilities, including GenAI, AI, and some of the natural language processing models. Their experimentation in this area is a really good thing and it highlights how rapidly some of these technologies are being adopted.

David Gritz

One challenge startup MGAs have (versus established insurers) is that they don’t necessarily have longitudinal data or a big store of data because they’re just getting started. We have a company in our lab, Parachute, that uses SBA loan data and data from public entities to establish policy rates and values for family offices that invest in private equity or other individual private companies. But for MGAs that can’t identify an applicable public data set like this, they are actually at a disadvantage.

Denise Garth

And, it isn’t just that they need a good repository of historical data that can only come through time, but nearly two-thirds of MGAs don’t even have access to their own operational data. That’s the fuel for core operational knowledge. Do you have access to your underwriting data, your policy data, your billing data, maybe even your claims data, so that you can begin to look at it? This data is the foundation of AI capabilities.

MGAs need to look at their technology solutions to make sure they have access to that data.

David Gritz

This is definitely a blind spot for a number of MGAs — the full life cycle. If you can look back at the past one to five years of claims, you can take advantage of what you learned next year when you update underwriting guidelines. If you’re writing auto, what are the trends that are changing? If you’re on the property side, how does the shift in Tornado Alley affect the book of business you’re already committed to?

In Summary:

- MGAsare in a leading position to meet the demands of a shifting market landscape.

- They need operational model agility to respond to market conditions, speed to market for new products, and to create a technology foundation that includes next-gen intelligent core and AI for optimized operations and market agility.

- MGAs are behind in replacing legacy solutions. This one thing places them at a disadvantage to new MGA startups leveraging next-gen intelligent solutions.

- MGAs are increasingly using data analytics for underwriting profitability.

- Emerging risks and demand for more specialized, niche products offer significant growth opportunities.

- MGAs leverage distribution strength and outpace insurers with a multi-channel focus and lead the embedded insurance market.

- MGAs are creating a significant gap with insurers by focusing on the agent experience, potentially shifting where business is being placed and creating market dominance.

David Gritz

If the advantage that MGAs have is nimbleness and attentiveness to customers, then they have to build the infrastructure to be able to provide that on a continuous basis. They need to have the right technology to make it seamless, and get access to use the data that they have or to augment with third-party data. Then, they need to take advantage of these trends with machine learning and generative AI to stitch together the pieces that don’t natively work.

Denise Garth

The future is extremely bright for MGAs. Those who are on a path of establishing an agile operating and next-gen intelligent technology foundation are poised for future growth. There is a lot of opportunity for those who are beginning to think about how they transition from the way they’ve done business for the last 10 or 20 years, to really take advantage of a very different risk and market environment.

Thank you so much, David, for all of your insights and input. For a deeper dive into MGA perspectives and opportunities, be sure to read MGAs’ Strong Growth and Growing Role in the Insurance Market: Strategic Priorities 2025 and for additional conversation on the future of AI in insurance, be sure to sign up for our upcoming webinar, AI Horizons 2030: What Will an Autonomous Age Look Like? A view post ITC 2025!