Blog

Insurance Transformation: Is the Current Business Model at a Crossroads of Change?

Insurance transformation is a business imperative, not a technology project. Without transformation, insurers will find themselves stuck with tools and processes that do not match reality. Risk, claims, and operational costs are all on the rise. Only a business model and technology foundation change can help insurers avoid permanent damage. Because business-as-usual is no longer viable.

Why are insurers replacing core systems now?

Circumstances, industry shifts and priorities are forcing insurers into motion. Diminishing loyalty among customers isn’t a random anomaly; it is the direct result of increased pricing caused by increased claims costs, rising operation costs and out-of-synch operating models. Growth has stalled. The risk landscape is now consistently inconsistent. The core system sits at the center of changes that are strategic and necessary. Intelligent core systems enable business model response to change.

The way forward must include both operational, technology and innovative initiatives that redefine and drive the transformation required for not just today’s business, but the future business. Doing so can bend the cost curve that drives profitable growth and operational efficiency and creates competitive differentiation to acquire and retain customers—and manages the growing need for talent.

Majesco’s recent Thought Leadership report, Leaders Reinventing Insurance: Strategic Focus on Business Operating Model and Technology Foundation, outlines the strategic initiatives that have the highest impact and which insurance transformation trends add value to the business.

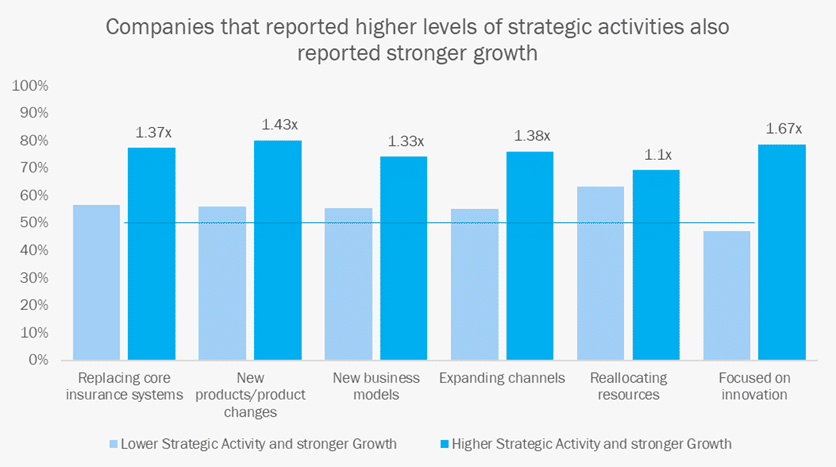

Six strategic activities insurers should execute

Business operating models need flexibility, scalability and the technology capabilities available now with intelligent core systems. Insurers with materially stronger growth report higher engagement with the six strategic activities as seen in Figure 1, highlighting the growing shift away from business as usual. These include (ranked by impact):

- Innovation (1.67x)

- New products/product changes (1.43x)

- Channel expansion (1.38x)

- Core replacement (1.37x)

- New business models (1.33x)

- Reallocating resources (1.1x)

They all show a consistent upside and business value impact for leaders as compared to their lower-activity peers – followers and laggards. And they are interrelated to maximize the impact on growth. So, the idea of selecting just one or two of these strategic activities as a point of focus is not impactful.

These strategic initiatives should be considered the six pillars within a new operating model and technology foundation. To achieve the business value of transformation, insurers must execute broad structural moves and operating discipline, not incremental tweaks or occasional initiatives.

Growth isn’t accidental; it’s earned through deliberate strategy and execution. This isn’t just a nice idea; it’s a measurable advantage. These strategic multipliers are direct drivers of growth that compound over time, creating a widening gap between those who act and those who don’t.

Also worth mentioning: Budget shifts alone, without aligning to a strategy, initiatives and execution, will not move the needle for success.

The key takeaway for leaders: Stop separating “growth strategy” from “execution strategy.” These six strategic initiatives are an interconnected foundation where modern intelligent core enables operational efficiencies with access to all data; leverages advanced analytics (including AI); creates speed to market and expand market reach; empowers innovation that creates competitive and differentiated value; and reallocates resources to invest in high-value and high-growth initiatives. Together, these strategic initiatives accelerate business momentum that aligns with the strategy, rather than episodic bursts that react to the moment with minimal sustaining value.

Figure 1: Strategic activities’ impact on growth

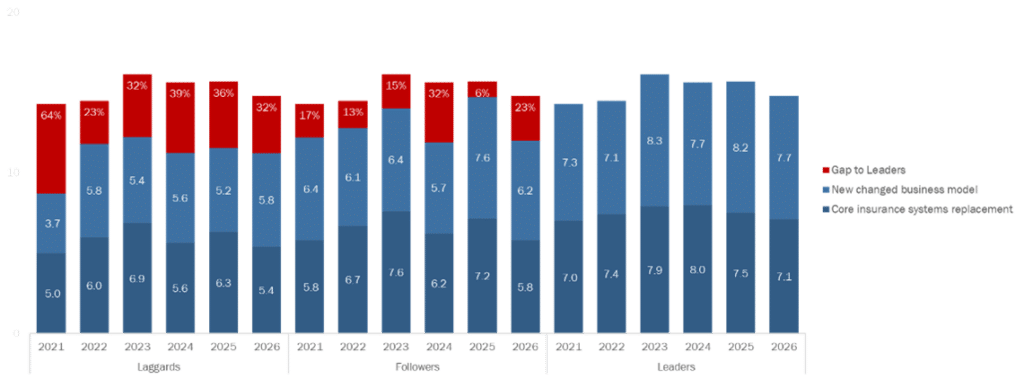

When looking at these strategic initiatives year over year, there is a persistent, widening gap between Leaders and the rest of the market, as seen in Figure 2. Leaders demonstrate consistent, higher momentum, while Followers slip and Laggards remain constrained, placing them at a continued widening disadvantage, underscoring significant structural differences.

The pattern is particularly concerning based on two key foundational elements: business-model change and legacy core replacement, which reflect a business-as-usual mindset. In a challenging market environment defined by cost pressure, volatility, new tech, and intensifying customer and channel expectations, the gap represents a growing operational and strategic risk accumulation reflected by: process and manual workarounds, slower time-to-market, constrained data access and AI adoption, mounting talent friction, and increasing operational costs.

Figure 2: State of business model development and core systems replacement by Leaders, Followers and Laggards

How do insurers align technology and operating model investments?

Leaders are executing business model change and legacy core systems replacement as synchronized programs. Modernization without operating model redesign yields limited ROI; operating model ambition without Cloud and AI native platforms ends in the realization that without them, nothing really changes.

Ultimately, success is a matter of road maps and a mandate to prioritize alignment. Investment roadmaps for the operating model and technology needed. Tech partner selection and alignment are crucial to ensure they will align with the strategy, transformation, and innovation priorities. Insurers will want to select partners based on strategy, innovation focus, and financial strength and avoid InsurTech Zombies that put their business at risk. The right partner means the difference between business success and failure over both the short and long term.

The right tech partner will unlock new operating capabilities and business model moves that will empower the business by propelling profitable growth, higher performance, and increased competitiveness. Keeping the operating model and the technology aligned pays off when both are up and running with reduced friction and a new “feel” of business that was built to succeed.

Optimism Sentiment: Signposts at the Crossroad of Change

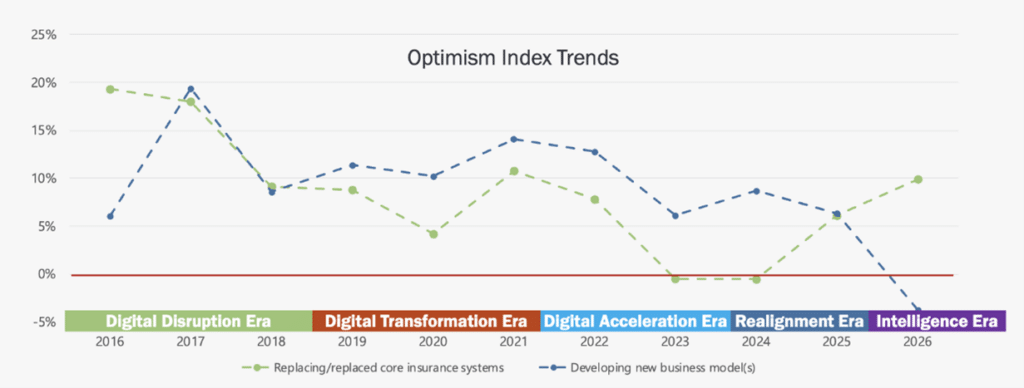

As the pace of change in the insurance industry continues to accelerate, often beyond what traditional strategic and operational planning can keep up with, there is a decreasing level of optimism. Across the multi-year optimism view in Figure 3, expectations for both legacy core replacement and new business model development have trended downward year-over-year, reflecting the challenges of the pace of change, financial stress, market shifts, and technology emergence.

For the first time in the research, business model optimism was negative. With so many issues challenging the industry — economic, demographic, technological and new risks — the fragility of the traditional operating model has become front and center. Rethinking and reinventing the business operating model has never been more needed than now. The old methods of modernization did not achieve the business results required. Insurers lacked focus and thought the “secret sauce” was customized business processes. The result was increased software and operational costs, limited agility and ability to quickly upgrade to leverage new innovations. It increased business and strategic risk.

In contrast, legacy core system replacement shows a significant upswing, reflecting a growing understanding that cloud and AI native core technology is the enabler of business and operations reinvention and improvement. Insurers can take advantage of embedded intelligence and automation, particularly with GenAI and Agentic AI, that provide out-of-the-box optimized business processes which redefine the operating model of the past and encourage insurers to focus on what really differentiates them … their insurance products, underwriting, and channels.

Risk aversion is likely shaping the sequencing of the two together. Leaders are not waiting to “finish” rethinking their business model or starting their core replacement; instead, they are co-designing the two together: modernizing core and data architectures in the service of specific business model outcomes—faster product development, ecosystem distribution, AI-driven underwriting and servicing, elevated experiences, and lower-cost operating models.

The leadership takeaway is that they must be done together, not separately. Leveraging cloud and AI native core system capabilities as the basis of a new operating model accelerates transformation and creates a foundation for continuous reinvention. A litmus test for new core systems is a peek into the future. When new capabilities and innovations are available, will the new core systems handle them?

Figure 3: Optimism index trend – Core Systems & Business Models

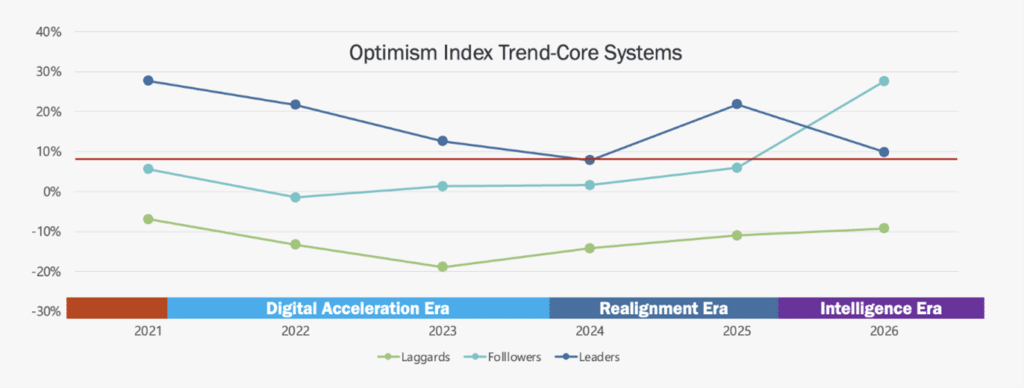

Reinforcing this leadership view, Leaders reflect strong optimism as compared to Followers and Laggards, as shown in Figure 4. While Followers oscillate around neutral with an unusual positive spike this year, the overall gap as compared to Leaders remains material—suggesting intent without full commitment, or commitment without a strategy and the execution muscle to believe in outcomes. Will this spike of optimism create the change needed? Time will tell.

Laggards are consistently negative and deteriorate sharply this year. The severity of their negative optimism is not just a mindset issue; it reflects the intensifying business challenges due to constraints of high technical debt, complex integrations, prior modernization failures, and limited ability to fund multi-year programs while under growth and profitability pressure.

This is precisely why this pattern matters: pessimism becomes self-fulfilling when it leads to delayed decisions. Delayed decisions further increase the eventual cost of modernization and decrease business growth. At the crossroads of decision, business transformation will reset insurer paths, providing more optimism and satisfaction to the business while improving business metrics and meeting the protection needs of their customers.

For Leaders, this represents a competitive window of opportunity. If peers choose to hesitate, the payoff for building an evergreen operating model and cloud- and AI-ready core foundation increases by unlocking faster product iteration and competitive advantage, enhanced data access and business insights, and operational optimization with deployment of GenAI/agentic AI workflows.

Followers and Laggards need to reassess their strategy and execution in terms of transformation scope and speed to retain any opportunity to compete and remain relevant. Waiting only creates more pain and cost.

Figure 4: Optimism index trend – Core Systems, by Leaders, Followers, and Laggards

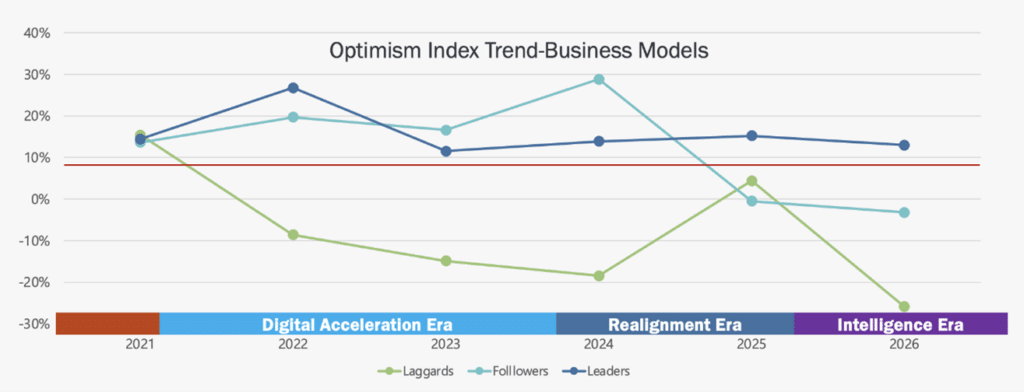

Business model optimism reflects even greater volatility and divergence than core systems replacement, as seen in Figure 5. Leaders remain relatively consistent, but Followers and Laggards both drop significantly into negative territory.

This pattern reveals the challenges faced by Followers and Laggards in business model reinvention—harder, riskier, and more uncertainty on technology. As the industry enters an “Intelligence Era,” where differentiation depends on operating model redesign, next-gen intelligent core, ecosystem/channel innovation, and new forms of product value, Followers and Laggards are increasingly falling behind.

Followers’ and Laggards’ negativity implies a dangerous mix of uncertainty, constraint and reluctance, often driven by the belief that the current business model can be optimized enough, and that change is not happening that fast.

In today’s reality, those assumptions are notably invalid and highly risky. Expense pressures, market competitiveness, scale and agility demand, and customer experience expectations are only intensifying from AI-enabled competitors, which makes “incremental transformation and optimization” a losing strategy. It will not keep pace, putting them further behind the Leaders.

Figure 5: Optimism index trend – Business Models, by Leaders, Followers, and Laggards

Leaders will likely be executing relentlessly with measurable business outcomes. Followers and Laggards are at a crossroads. They need to define a strategy to rethink their operating model and technology foundation with a focus on relentless execution, rather than treating the change as an abstract aspiration.

Where does your organization stand?

Your business operating model needs to change, and your technology foundation needs to support it.

The business, however, is often slow to move and cautious about major initiatives. “Our thoughtful, measured approaches of the past have worked. Why change the process? Past implementations took years. Everyone accepted it.”

At the crossroads of tradition and innovation, Majesco can help your company to choose a course that includes both. We honor your unique culture and position in the industry AND can accelerate your business model change and its positive results. We open the curtains to your forward-thinking development teams and help to unify your enterprise behind a whole new approach. Is it time to move out of the crossroads and take a new path forward? Contact us today. For more evidence on how business operating models and technology foundations have an impact on insurers like you, be sure to read, Leaders Reinventing Insurance: Strategic Focus on Business Operating Model and Technology Foundation today. Capture more ideas for innovation with Majesco webinars, including our latest, Closing the Insurance Customer Protection Gap: How Generational Difference in Risk, Readiness, and Coverage are Redefining Insurance Value