Blog

More With Less: Using AI to Improve P&C’s Elusive Expense Ratios — A Benchmarking Study

In the early 1990’s, Toyota Motor Company had achieved a great deal of success, and it was experiencing the benefits of an excellent economy and top-notch engineering. Its products were good. Its manufacturing technology was state-of-the-art. Its processes were stable and efficient. According to Toyota historian Jeffrey Liker, “the biggest crisis, from the perspective of Toyota leaders, is when associates do not believe there is a crisis or do not feel the urgency to continuously improve the way they work.”[i]

So Toyota began researching cars for the 21st century…homing in on a project called G21, which would later be known as the Prius — the first mass-produced hybrid car. Project G21 had two goals. 1.) Develop a new method for manufacturing cars for the 21st century and 2.) Develop a new method for developing cars for the 21st century.

In nearly any case, developing a new product with entirely new technology would normally take twice as long as developing one using existing technology. In the case of G21, Toyota invented entirely new processes for development that cut standard “blueprint to production” time in half. The result: faster innovation, faster manufacturing, improved profitability, and greater market penetration.

As executives consider use cases for GenAI and Agentic AI for P&C insurers, the possibilities are limitless. However, insurers should be careful to view these in the proper context. AI can improve individual processes, but a broad, strategic approach that looks at establishing the foundation of leveraging GenAI across the entire value chain will unleash the full capabilities of faster innovation, faster product development, faster quote to bind, faster service, improved operational costs, and greater market penetration. Leaders should envision an entirely new business.

They should consider the details of specific use cases, but grasp that the full realm of development and delivery will provide a more impactful combination that lays the groundwork to rethink and create value across the entire value chain. For an in-depth look at the potential of AI in insurance, based on Majesco benchmark studies, be sure to read the thought-leadership report, A Powerful Chain Reaction: The Financial and Operational Impact of GenAI and Agentic AI Across the Insurance Value Chain.

Optimizing and Strengthening the Insurance Value Chain

As we pointed out in our recent Avoiding Operational Chaos blog, insurers who think strategically—rather than tactically—can unlock compounded benefits that far exceed the sum of individual task improvements.

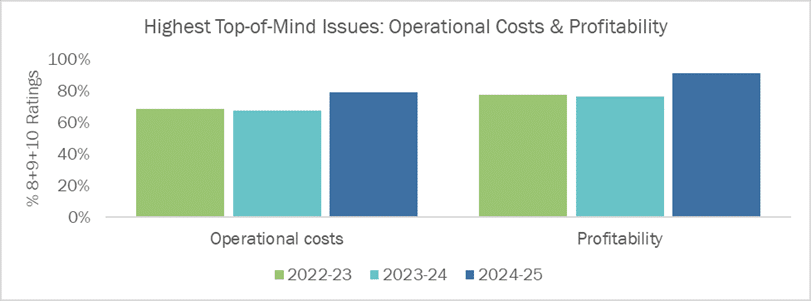

The demand and need to drive down operational costs and improve profitability are underscored in our 2025 annual Strategic Priorities research, which found both to be insurers’ most important top-of-mind issues the past three years (Figure 1), highlighting the real opportunity for AI. And our early assessment for the 2026 Strategic Priorities research puts operational costs, advanced analytics and profitability as the top three top of mind issues, further highlighting the opportunity for AI.

Figure 1: Insurers’ most important 2025 top-of-mind issues

Survey question & scale: How important or top of mind are these topics to your company? 1=Not at all; 10=Very much

Reducing operational costs in areas such as claims, underwriting, billing, and policy administration not only improves operational efficiency, which substantially impacts insurance expense ratios and, in turn, strengthens overall financial metrics. End-to-end process optimization leads to leaner cost structures, which lead to improved profitability, combined ratios, and competitive pricing.

GenAI and Agentic AI for P&C insurance are ushering in a new era of intelligent and optimized insurance operations—one where processes are efficient and effective, decisions are data-driven, and employees are empowered with real-time insights and automation to elevate the customer experience that will drive retention and loyalty.

P&C Current State

After several turbulent years, the U.S. property and casualty (P&C) insurance industry posted a significant financial rebound in 2024, largely driven by a sharp turnaround in personal lines due to increased pricing for both personal and commercial segments.

Insurers’ aggressive rate and pricing increases, ranging from 10-50% each year, to improve underwriting and profitability metrics and help financials, have had a counter-effect on insureds, resulting in switching to insurers with lower costs, reducing coverages, increasing deductibles, or eliminating insurance coverage. This result is counter to the purpose of the industry and is now creating a growing protection gap of risk and negatively impacting trust and retention. This is unsustainable for everyone.

Older auto policy shoppers — The most loyal become the least loyal.

At one time, the youngest generation of auto policy shoppers were those most likely to shop their policies around, while the older “traditional” insurance buyers were the most likely to remain loyal to their insurance brand. Now, those in the 56-66+ categories have the highest shopping growth rate.[ii] While policy shopping can be great for brands that are ready to convert prospects into policies, for other insurers, this trend can quickly lead to policy declines and profit loss. Price increases should be one component in a holistic plan for profitability. Where does operations fit in the balancing act between insurer profitability, customer satisfaction and retention?

Despite 2024’s combined ratio improving to 96.6 from 101.6, expense pressures and increased risk persist, with loss and loss adjustment expense (LAE) costs rising slightly, and underwriting expenses increased nearly 10%.[iii] The industry is doubling down on rate adequacy, risk selection, underwriting and claims management to contain costs. What is missing is the focus on the broader operational costs and expense ratios, which can drive profitability, market competitiveness and customer satisfaction.

AI as the Expense Ratio Game Changer

Implementing Gen AI and Agentic AI across the value chain empowers insurers to regain more control and business value. Using it to complete service or quoting requests at a quicker rate, allowing insurers to get more done with less staff, or helping them meet increased demand and prioritize submissions that can drive new levels of optimization and profitability without needing to hire more staff.

With an increase in shopped policies, submission rates become a real issue. Insurers are getting swamped with requests. Those running traditional systems may find it difficult to cope. GenAI and Agentic AI, however, will enable them to not only meet the demand but also prioritize the submissions that can provide them with the most profitability.

Success requires leadership and the willingness to rethink the business. We see these key characteristics of AI, GenAI and Agentic AI Leaders:

- Concentrate on core business processes (underwriting, policy, billing, claims) for competitive advantage

- Emphasize people and processes over technology to rethink the business

- Move beyond operational productivity to revenue, profitability, and employee empowerment

- Invest strategically in key areas to scale and maximize the value of AI and GenAI, advancing broader investment and moving quickly to Agentic AI

P&C Benchmarking with AI, GenAI and Agentic AI Looks at the Details of Expense Ratio Reduction

The P&C insurance value chain and opportunities to leverage AI, GenAI and Agentic AI are broad and will be a game-changer. Instead of discussing these at a high level, however, Majesco sought to examine operational efficiencies in fine detail. The details are the proof points. Here is what we found.

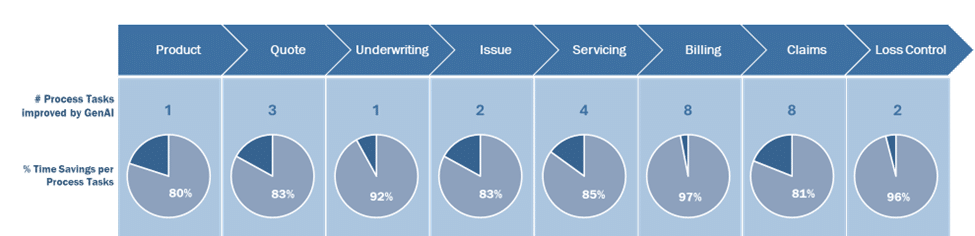

Figure 2 highlights the high-level P&C insurance value chain with the number of current use cases for these actionable tasks and their average time savings within each process that Majesco has ready and available in the P&C Intelligent Core Suite. Each of the use cases has been benchmarked with and without GenAI or Agentic AI for actual time savings.

Figure 2: Number of Current GenAI-Aided Use Cases and Average Time Savings: P&C

Because each company’s business is different in terms of products, organizational structure, jobs and business volume, we have estimated the time savings per task with an “illustrative hours” saved per day and year based on an assumed number of tasks each day for a single individual

To transfer these estimates into your own company’s situation, estimate your specific time savings based on your business, then correlate that to your cost per hour for that role and the number of people performing it to calculate the ROI business value potential.

Based on these details for each high-level core business process and illustrative examples (excluding Loss Control), an insurance company using Majesco’s P&C Intelligent Core with the current use cases based on a single transaction and user could save 98,787 hours annually.

Assuming an average annual workable time of 1,700 hours per FTE and an average salary of $70,000, the baseline would save the time of 58 people at $4,067,711 across the value chain as a baseline.

These numbers do not include efficiencies in answering questions using embedded GenAI with Majesco Copilot, which answers questions on how to use the product through natural language, eliminating the need to refer to and search the online User Guides. This could reduce training costs, help onboard employees faster and ensure consistency in the work. Users can simply type what they need help with, and Copilot searches the extensive online library to answer the question.

Majesco Copilot can provide information for users regarding specific customer or policy information, helping to improve productivity, consistency and quality in answering questions. A 360-degree view of a customer is easily accessible from coverage to bills and claims, to what other coverage is available. Copilot can also answer questions anywhere from why an overpayment was created to understanding reserve status!

Using the same assumptions, companies using Majesco Loss Control would save the time of 6 FTEs at $439,923 annually.

More importantly, this baseline would substantially increase when applied to the true number of people, the number of tasks performed daily and their actual salaries, raising the potential savings well into large six and seven-figure figures for many companies.

Depending on the company, it is not unrealistic to consider a minimum of 2% – 5% impact on the insurance expense ratio – either through reduction of cost or by processing more at the same level of staffing.

Details of specific use cases in the value chain areas for P&C are detailed in the full report. And these use cases are growing quickly.

A new equation — maximizing operational resources.

Majesco is leading the industry in the use of AI, GenAI and Agentic AI embedded in all our core solutions. It’s not just a technological upgrade. It is breaking barriers and creating a new era of operational excellence. Majesco Copilot is available on every screen of our solutions, providing the ability for users to ask basic questions such as how to do a transaction, summarize information, draft a reply and more. These general capabilities leverage the embedded online documentation and data within the system.

In addition, Majesco has developed more in-depth capabilities with GenAI and Agentic AI agents that go beyond the ability to provide transactional guidance, summarize information and accelerate routine administrative tasks, by assisting in actionable tasks and transactions. Every day, using AI’s ability to grow into its role, Majesco’s Intelligent Core solutions are gaining in their ability to impact profits by reducing insurance expense ratios.

Of course, the details given in benchmarking can help us with examining hours saved and costs saved in FTEs over time. This is the financial perspective. But what shouldn’t be forgotten is that faster, more efficient processes lead to a much shorter timeline — greater service in-house, better service to agents and easier transactions with end customers.

Though benchmarking is “just a start” in the conversation, it can give insurers clarity and a forward-looking vision of their future state. How far can AI take an insurer’s operations? The reality is that there is no limit. Constant improvement within operations will become the norm for companies that embrace AI throughout the P&C value chain. The most important step is the first one. Are you ready to take it?

For more information on the operational efficiencies available to your organization, be sure to read A Powerful Chain Reaction: The Financial and Operational Impact of GenAI and Agentic AI Across the Insurance Value Chain.

[i] Liker, Jeffry K., The Toyota Way, p. 51, McGraw Hill, 2004

[ii] Batiste, Jeff, “LexisNexis Insurance Demand Meter — Trends from Q3 2025,” LexisNexis, November 19, 2025

[iii] Coppola, Matthew, “First Look-First Look-2024 US Property-Casualty Financial Results,” AM Best, March 18, 2025