Blog

Insurers’ Top of Mind Issues Shift Technology Focus for 2026

“At scale” is one of those unique terms that business and technology consultants have slipped into the business lexicon under the radar. But then the phrase took off, gaining in meaning as companies gained the need for scalability. At scale became a descriptor, a goal and a rallying cry. It is no longer enough for systems and processes to be expandable. We need them at scale and right now.

In fact, the term “at scale” has an impatient subtext that current processes are too limited, confined, and too late. If we ask the tough questions to the business, such as “What is limiting us,” maybe we have “at scale” to thank for pointing us in the right direction.

Limits hurt business. Non-scalable platforms, legacy processes, and workflows limit the business. No one aims to limit a business model; however, decisions to customize the technology, manual workarounds, and previous focus on bringing forward legacy business processes are now placing significant limitations on the business and how it operates. Previous advancements, such as point-to-point application interfaces, were helpful. They carried the data where we needed it. Over time, though, some of these gave us coding nightmares, elongated update timeframes, and scalability headaches. Yesterday’s building blocks became today’s tripping stones. Innovation became limited.

Today’s operations must be able to trust that systems can operate with agility, speed and at scale.

Insurance industry operating model transformation cannot be accomplished without the idea and fulfillment of the business at scale from underwriting and products through service, billing and claims as a future-ready enterprise where every aspect of the insurance value chain can run at scale when it needs to. This requires a new kind of insurance technology transformation that looks further ahead into the future as it addresses today’s pressing issues.

As it stands, most insurers are ready to embrace this kind of technology shift. In Majesco’s recent strategic priorities survey of insurance executives, we found thatthe distribution of this year’s top-of-mind issues paints a clear picture of an industry still grappling with fundamental operational business model pressures as well as technology foundation challenges. These pressures are laying the groundwork for both an operational business model and technology platform change.

To look at the picture more closely, be sure to read our recentthought leadership report, Strategic Priorities 2026: A New Era of Innovation and Disruption Offers Real Business Value. This blog looks at how these new areas of focus are rewriting the insurance technology story to include a much broader and comprehensive look, fostering AI, GenAI and Agentic AI usage by getting a better grip on data and aligning systems to operate at scale.

Insurance Industry Challenges

Most insurance operating models were crafted over decades around a myriad of constraints, business assumptions, legacy practices, and challenges. The operating model evolved over time to support a legacy construct by layering in technologies over legacy processes and technology with the hope of optimization. Much of this resulted in inefficient, unprofitable, and employee-constrained operations that increased costs rather than decreasing them for both the business and IT. It’s time to right the ship.

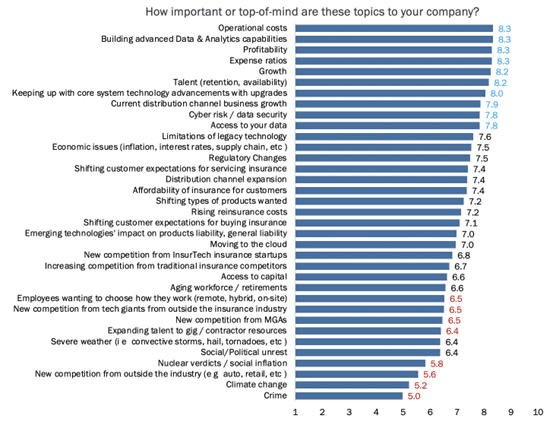

Insurance executives indicate a laser focus on operational costs, profitability, expense ratios, and growth, which, in the Majesco Strategic Priorities survey, all score above 8.0 on a 10-point scale as seen in Figure 1, placing them at the very top of insurers’ agendas. The rating pattern reflects a continuation of last year’s financial strain, including inflationary pressures, elevated loss costs, ongoing reinsurance rate increases, and the continuing impact of catastrophic weather events. The close clustering of the top issues indicates broad, sector-wide agreement that efficiency, financial performance, and cost structures are significant concerns.

Technology themes — including advanced data & analytics (8.3), keeping up with core system advancements (8.0), and navigating limitations of legacy systems (7.6) confirm core systems modernization in insurance is no longer viewed as a strategic luxury but rather a necessary enabler of financial outcomes. The cost and impact of legacy debt are poisoning and pulling organizations down.

With increasing retirements and loss of institutional knowledge and skills, operational risk is rising due to the difficulty in accessing and leveraging the data for insights, decreased operational productivity due to manual workarounds, lack of speed to market for new products, and the inability to use new technologies like GenAI and Agentic AI to drive operational optimization, and legacy debt.

In fact, legacy technology increasingly is a hindrance and harbinger of declining growth and competitive edge. It hinders insurance business strategy. Legacy tech is an unstable foundation, negatively impacting operational efficiencies, cost ratios, and profitability, along with constraining talent and limiting access to data.

Customer expectations for service (7.4), products and buying experiences (7.1), distribution dynamics (7.9), and talent availability (8.2) fall just below the technology tier, signaling that while experience and workforce challenges remain pressing, they are exacerbated by operational and technology constraints.

In the lower third of rankings, scoring below 7.0 yet above the 5.0 midpoint, insurers reveal important, but less urgent, issues that reflect emerging pressures and long-horizon risks. Competition from InsurTechs, traditional incumbents, MGAs, and even tech giants appear in the mid-6 range, suggesting that while competitive disruption is acknowledged, it is not currently viewed as an immediate threat.

Similarly, concerns related to workforce shifts, hybrid work preferences, access to capital, and economic uncertainty sit in the 6.0–6.7 range, indicating steady but not critical pressure.

Interestingly, several systemic external risks—including severe weather, social/political unrest, nuclear verdicts, crime, and climate change—fall near the bottom of the list, despite their growing impact on underwriting profitability, volatility, and reinsurance costs.

Overall, top-of-mind issues reflect pragmatic, fundamental challenges of today’s business operations that must be addressed to compete, let alone survive, as we rapidly enter this new era of insurance.

Figure 1: Insurers’ Top-Of-Mind Issues

Likewise, the year-over-year changes in the technology subset highlight a meaningful uptick in the urgency around next-gen data and technology foundations. The most striking movement is the 10.1% increase in importance for building advanced data and analytics capabilities. This surge underscores how quickly AI, particularly Generative AI and Agentic AI, has shifted from experimental to operational and strategic necessity. If anything requires a completely new approach with an “at scale” mandate, it is data and analytics. Capitalizing on AI, GenAI and Agentic AI cannot be accomplished without this shift — and insurance executives know it.

Insurers increasingly recognize that without AI and cloud-native solutions with strong data foundations, AI capabilities are often not achievable, let alone scalable. In addition, regulatory scrutiny will intensify and critical improvements in underwriting, servicing, claims, and pricing will remain limited. The fastest way to modernize legacy insurance core systems quickly will be to ‘go AI and cloud-native’ and ‘get the data house’ in order.

The 6% rise in technology importance overall, paired with a 4.8% increase in keeping up with core system advancements, reinforces the industry’s acknowledgment that legacy systems are now obstructing efficiency, talent strategy, innovation and profitable growth, key reasons that must drive legacy replacement now, not in 3-5 years. At scale is a rallying imperative.

Table 1: Year-Over-Year Changes In The Top-Of-Mind Issues Technology Subset

In an environment where underwriting complexity, pricing pressure, operational costs, and claims volatility continue to rise, treating data and technology as a strategic foundation, rather than a supportive one, will determine which organizations can truly modernize their operating models, cost structures, create innovative products, proactively address risk, and meet customers’ escalating expectations. Replacing legacy core technology with next-gen intelligent core that is AI and Cloud-native has never been more important.

Lowered Expectations, Decreased Optimism

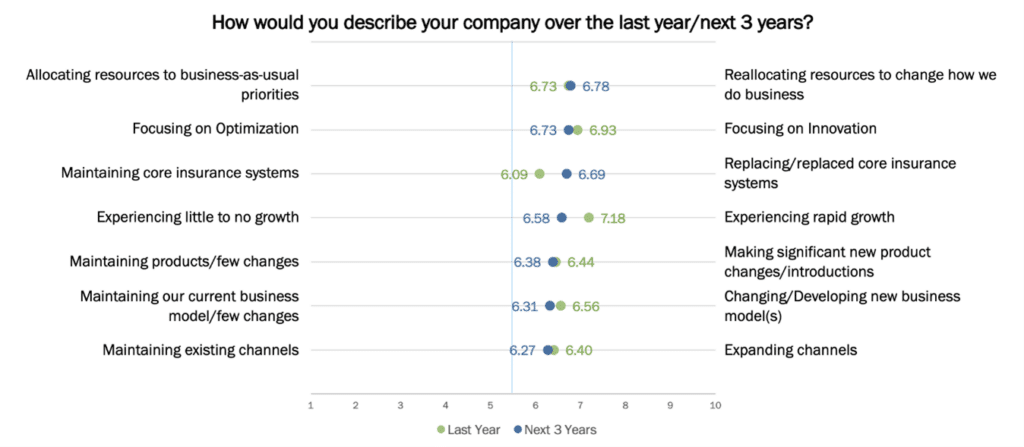

The comparison between the assessments of companies’ performance last year and their outlooks for the next three years in Figure 2 reveals a cautionary signal: several forward-looking expectations are flat or lower than the assessment of the past year, suggesting a downturn in organizational optimism.

While some activities show modest increases — such as reallocating resources to change how the business operates (6.7 to 6.8) and modernizing core systems (from a low 6.1 to 6.7)—a number of others decline or remain unchanged. Expectations for strong or rapid growth fell from 7.2 to 6.6, indicating reduced confidence in future market growth. Innovation declines slightly (6.9 to 6.7), signaling that, despite recognition of innovation’s importance, insurers see real constraints on their ability to execute.

Product and business model evolution remain stagnant or in decline: significant new product changes hold flat at 6.4, while expectations for business model change slip from 6.6 to 6.3. Even channel expansion—historically a growth lever—dips from 6.4 to 6.3. These patterns collectively point to a sector that is much more restrained in its future expectations than in previous years. This is likely because of the constraints due to delayed action on modernizing their business models and legacy technology.

Figure 2: State of Industry Compared To Last Year

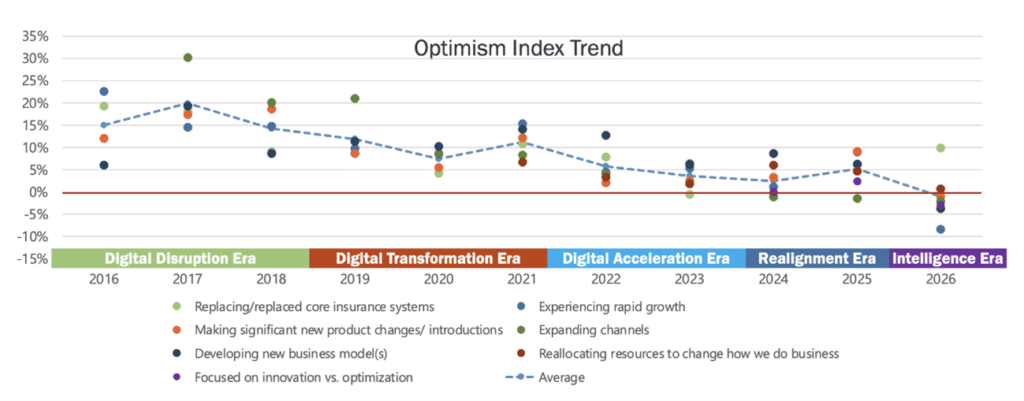

The multi-year Optimism Index Trend in Figure 3 shows a long arc that aligns with the industry’s major transformation eras, with 2026 being the advent of the Intelligent Era. This year’s data reveals a significant decline in forward-looking optimism for this era, reinforcing the same pattern observed in Figure 2 which highlights increased constraints. The magnitude of future optimism is significantly lower than in prior eras, with a majority of the categories hovering near zero or dipping negative—with experiencing rapid growth at nearly -10% — a substantial slide in optimism that reflects the gathering storm of challenges impacting insurers.

Key activities tied to business modernization—including channel expansion, new product introductions, and business model evolution—have significantly dipped except for core system replacement, which is the highest since 2020 when the shift to cloud-native core solutions gained momentum. This surge in core system replacement reflects the next major shift to intelligent core systems which are AI and Cloud native with embedded AI, including GenAI and Agentic AI that is recognized by the industry.

The downward tilt in the dotted-line average reinforces that the shift to the Intelligence Era highlights the tangible constraints on insurers’ ability to embrace this shift without both an insurance operating model and technology foundation transformation that leverages intelligence to new levels.

Figure 3: State Of Industry This Year Compared To Last Year

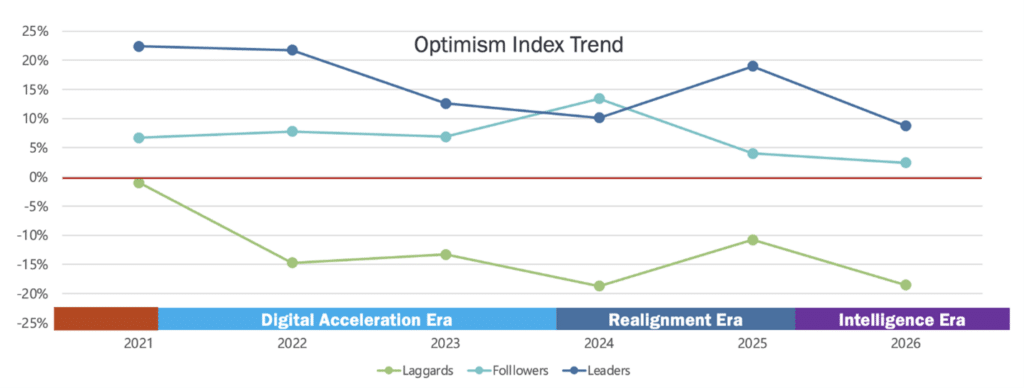

Looking at the optimism index by Leaders, Followers, and Laggards (Figure 4) underscores the wide divide between them and reveals a crucial theme from this year’s broader results: While Leaders continue to express higher optimism across all eras, today’s challenges and the shift to the Intelligence Era reflect a lower uplift for 2025–2026 as compared to the past eras. Once again, this highlights the magnitude of the impact of market and technology shifts, including AI and the lack of preparedness to embrace it.

Followers track slightly above the baseline but show a declining trajectory. Laggards remain the most pessimistic, with all years being negative and 2026 returning to the lowest level as seen in 2023. The decline aligns with the softening outlook seen in Figures 2 and 3, where forward-looking activity ratings for growth, innovation, channel expansion, and business model change were similar to or lower than past-year assessments.

Overall, the message is clear: confidence in the next three years is more cautious, more tempered, and more constrained than in past years, even among the industry’s most progressive insurers.

Figure 4: Optimism Index Trend By Leaders, Followers, And Laggards

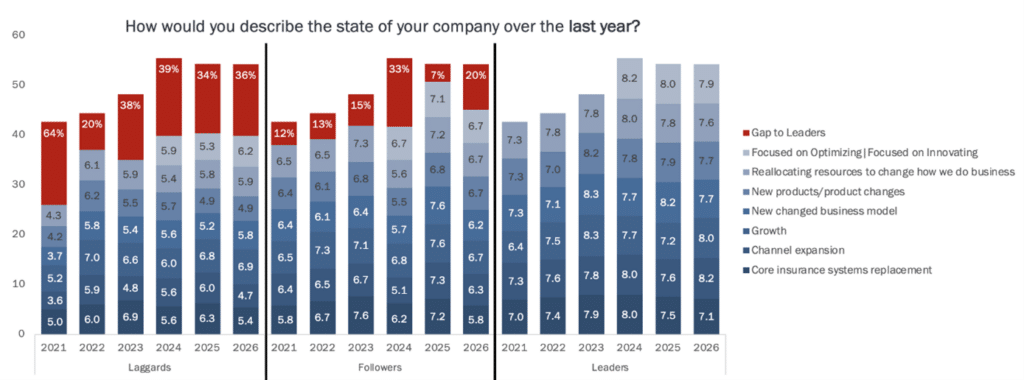

The striking gaps between Leaders, Followers, and Laggards reveal how each group performed over the last year. Leaders consistently report higher levels of activity across every strategic dimension—optimization, innovation, new product development, business model experimentation, channel expansion, and core system replacement. Followers continue to trail behind but saw a 13-point increase in their gap to Leaders this year, the second largest gap behind 2023, once again reflecting their inability to keep pace with the changes impacting the industry.

The most concerning is the entrenched stagnation among Laggards. Their activity scores are consistently significantly below Leaders, indicating limited or no meaningful action. The consistent large gaps to Leaders underscore how dramatically strategic inertia is holding back Laggard organizations, increasing their strategic and operational risk. Of particular concern is their low engagement in new products, business model change, and core system replacement—the very levers that enable modernization, resilience, and growth.

Figure 5: State of the company last year by Leaders, Followers, and Laggards

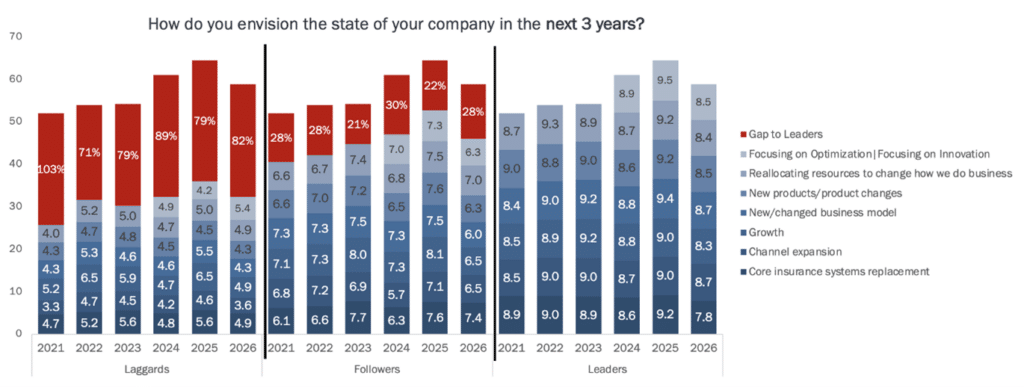

The three-year outlook dramatically widens the gap between Leaders and the rest of the industry.

Leaders project acceleration across every strategic dimension, with especially high expectations for innovation, business model change, product evolution, channel expansion, and core system modernization—reaching or exceeding the 9.0 mark. This level of activity highlights their focus on rethinking their business and technology to accelerate growth in the Intelligence Era.

Followers anticipate progress but at a more modest rate, while Laggards remain far behind, rarely anticipating major increases in activity. The resulting gap percentages, ranging from 71% to more than 100%, illustrate a future in which Leaders, Followers, and Laggards will experience completely different business and competitive realities.

Figure 6: Expected State Of The Company In The Next Three Years By Leaders, Followers, And Laggards

Leaders clearly grasp the benefits of switching to next gen core systems in insurance that will accelerate their ability to launch new products, expand channels, and implement innovation initiatives that will drive growth to new levels. In contrast, Followers will be behind, but still have the opportunity to refocus on these strategic initiatives and improve their business and competitive position to stay relevant. However, Laggards foresee, at best, marginal improvements, effectively locking in their gap and constraints that will hinder growth and market competitiveness, placing them at significant risk.

Moving from tech focus to tech action

It’s the tough questions that will drive insurers to make the necessary changes. What kind of stagnation and decline can we expect if we don’t change? How resilient is our business model if our legacy core systems and processes are inflexible? What insurance technology solutions are available to improve efficiency and allow for our business to thrive at scale?

Insurance industry operating model transformation begins with clarity around everything that limits an insurer and an understanding of technologies that liberate the operating model and its teams.

Where does your organization fall on the scales of technology focus? Is your position still foggy, or do you have clarity surrounding what it takes on the inside to foster growth on the outside?

At Majesco, we’re facilitating business and technology transformations that will place insurers on the right path to growth, efficiency, flexibility for the future and operations at scale for today. Our Insurance Data & Analytics solutions, which are embedded in our software to make them intelligent by leveraging AI, GenAI and Agentic AI, empowering access to all their operational data, and provides the foundation for their data strategy will prepare insurers for this new era of insurance that must adapt, innovation and scale.

Majesco is expanding and accelerating our investment in AI and aligned our tech development with both the needs of insurers and the timing of industry, demographic and environmental trends that will force insurers into new product and service offerings. Insurers can now make big steps in short periods of time to take advantage of an entirely new world of intelligent technology.

Optimism hasn’t disappeared. It is waiting to be harvested when insurers see what is available and decide to shift from focus to action.

Let Majesco show you what is possible. Contact us today and also be sure to find more deep insights in our Thought Leadership report, Strategic Priorities 2026: A New Era of Innovation and Disruption Offers Real Business Value.