Blog

Can Technology Solve the Insurance Pricing Conundrum?

Insurance’s emerging crisis may be affordability. Premiums for many insurance products are growing far faster than inflation due to changing and increasing risk, insurer profitability and other factors, creating affordability challenges for many customers which is leading to churning of business, decreasing coverages, eliminating coverages and more — increasing the risk for customers.

Pricing is a balancing act. With rate increases comes the risk of losing premiums and customers. If there is no innovation in pricing, soon, insurers should be prepared to lose policyholders and contribute to a growing insurance gap.

In the health market, for example, insurers are charging 26% more for coverage in 2026 than they did in 2025. With ACA premium tax credits expiring (a separate, but connected issue), health care marketplace enrollees could see their monthly health premiums double or triple.[i] In group health and voluntary benefits, the health increases impact where employees select other benefits products like critical illness, long-term care or disability.

Auto insurance premiums increased 35% between January 2022 and the end of 2024.[ii] Years of sustained losses for property insurers are driving up their prices as well. On average, premiums have risen 8.7% faster than inflation since 2019 — but significantly higher for many. From an insurance pricing perspective, geographic and risk variability is just one more issue that makes it difficult to price.

Inflationary and competitive conditions in the insurance marketplace are requiring organizations to evaluate aspects of their insurance pricing and underwriting, including operations and improved speed-to-market capabilities. The demand for regular or real-time updates for pricing will soon become mainstream. Currently, insurers find it difficult to quickly and efficiently update pricing and rating because of legacy solutions. Using a combination of modern pricing and rating engines, next-gen core systems, and new, innovative data sources and AI/GenAI capabilities, insurers can improve insurance pricing models, pricing speed, and accuracy and bring new products to market quickly — staying competitive and profitable.

Majesco Core Systems Research

As a part of our Strategic Priorities research, Majesco analyzed insurer core systems and their relationship to insurers’ business hurdles and successes. You can find greater detail on all insurer core systems in Majesco’s thought-leadership report, Strategic Priorities 2025: A Modern Era of Insurance Technology.

As a part of this study, we looked closely at current insurance pricing challenges as they relate to rating and pricing systems.

While auto pricing seems to be growing more stable, property and health-related products are still challenged. Given that a large percentage of insurers are still on legacy core solutions and may have multiples of them, they are challenged to quickly and efficiently update pricing and rating across these solutions, helping to ensure improved profitability.

At the same time, this creates customer challenges that require improved transparency, fairness, and accuracy in product pricing to maintain trust, a sense of value and, ultimately, retention with customers.

How can insurers “get granular” in their ability to categorize risks in order to soften increases among the lowest risks?

Data Sources

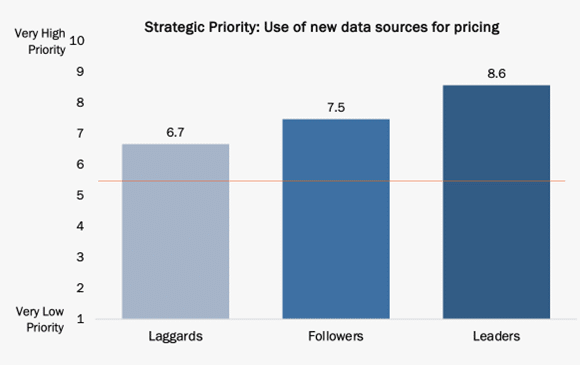

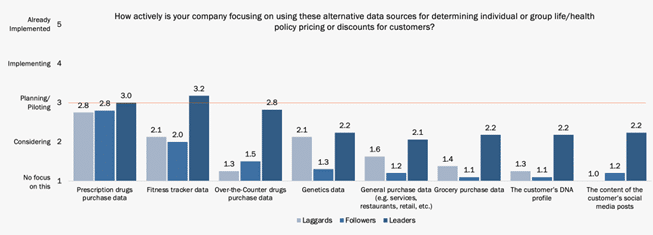

One way is to use new, innovative data sources from a customer to assess their specific risk, which can be used for personalized pricing. In Figure 1, all three segments (Laggards, Followers and Leaders) recognize the importance of using new data sources; however, Leaders outpace Laggards by 28% and Followers by 15% in terms of priority and likely execution.

Figure 1: Insurers’ priority for using new data sources for pricing

This leading position will differentiate Leaders in the market and attract a growing customer base interested in personalized pricing. However, there are differences among the three segments: auto, property and L&AH.

Auto Pricing

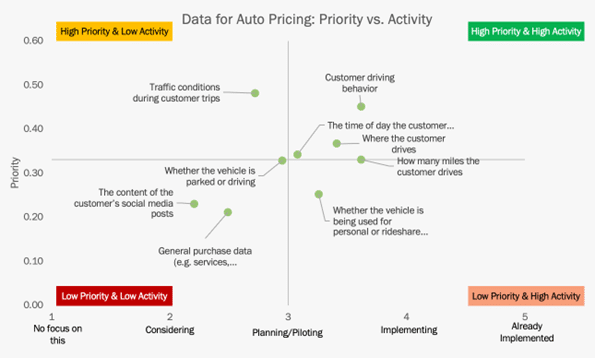

Adoption of connected vehicle data and telematics for auto insurance pricing is growing, with leading insurers taking a proactive stance in leveraging real-time driving data. Customer driving behavior, where and when the customer drives, and the number of miles driven all represent high priority and high activity, as shown in Figure 2. Other driving-related data categories are not far behind, but non-driving sources, such as social media posts and general purchase data, show low priority and low activity.

Figure 2: Insurers’ priority and activity levels in using new data sources for auto insurance pricing

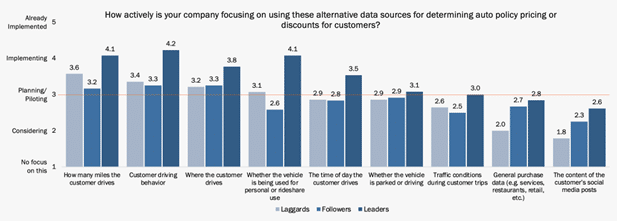

When comparing the three insurer segments, Leaders are well above or hovering close to the Planning/Piloting phase in all auto pricing data sources, with nearly 5 of them in the implementation stage. Competitively, they outpace Followers and Laggards in five of the seven driving-related categories, putting them at a great advantage given the growth in customers choosing telematics.

Surprisingly, Laggards are even with Followers on most of the categories, while leading them in two: whether the vehicle is used for personal or rideshare use (+19%) and how many miles the customer drives (+13%), putting them in a more favorable position competitively in the market.

Figure 3: Insurers’ activity levels in using new data sources for auto insurance pricing

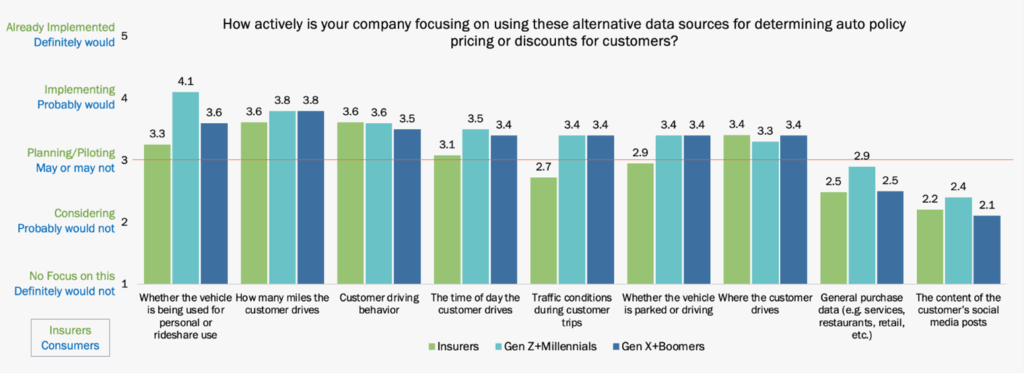

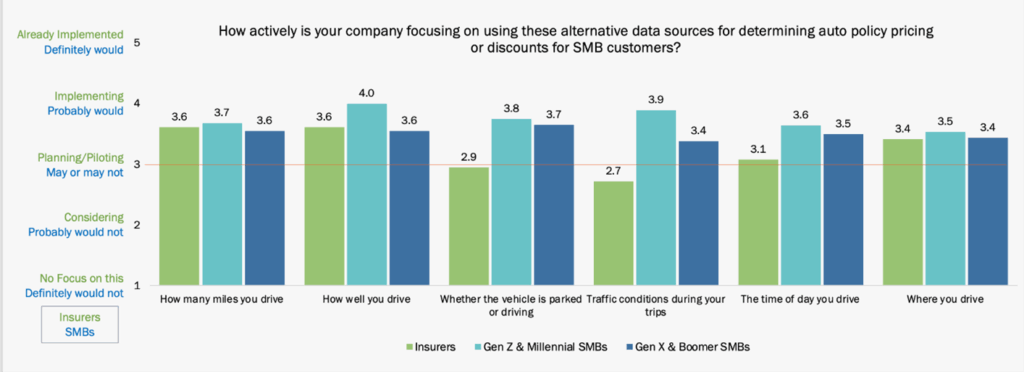

Our consumer and SMB research found that both Gen Z & Millennials and Gen X & Boomers are incredibly open to the use of personal data sources for their driving from telematics and connected devices to obtain a personalized rate. This includes miles driven, driving behavior, the time of day they drive, traffic conditions, whether the car is driving or parked, and where they drive, as shown in Figures 4 and 5.

Figure 4: Insurers’ activity levels compared to consumers’ perceptions on using new data sources for auto insurance pricing

Figure 5: Insurers’ activity levels compared to SMBs’ perceptions on using new data sources for auto insurance pricing

These interest levels are on par with or even higher than insurers’ interest levels overall. These all highlight the growing popularity and interest in UBI and telematics insurance. Given the dramatic increases in insurance prices that consumers and businesses have faced, J.D. Power anticipates a significant trend in 2025 for increased adoption of telematics-based pricing and usage-based insurance (UBI) policies that track driving patterns to offer discounts.[iii]

It makes sense, also, that it will be easier for insurers to use “instant” data, such as telematics, for faster changes to customer pricing. Good drivers, seeing quick improvements in pricing, are incentivized to continue their driving behavior.

Property Pricing

From 1980 to 2022, the annual number of billion-dollar disasters, adjusted for inflation, averaged 8.1. Over the past five years, the U.S. has averaged 18 billion-dollar disasters a year.[iv] The National Centers for Environmental Information has kept track of billion-dollar natural disasters since 1980 and cites increased exposure, vulnerability, and climate change as the reasons for the increase. It requires new thinking, new technology, data sources, and analytics to address the growing risk for insurers’ property portfolios.

Our 2023 Strategic Priorities research highlighted the lack of innovation in using new data sources for property pricing. Activity for every type of data was only at the Considering phase. Two years later, in the 2025 Strategic Priorities research, there are improvements in several categories.

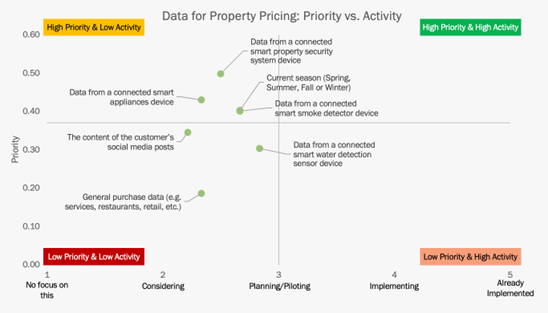

Season-based rates and data from different connected devices have a high priority but low activity levels, though they are within striking distance of Planning/Piloting, as shown in Figure 6. As noted, these options are popular with customers, reflecting a major opportunity for insurers and why they should accelerate execution and implementation.

Figure 6: Insurers’ priority and activity levels in using new data sources for property insurance pricing

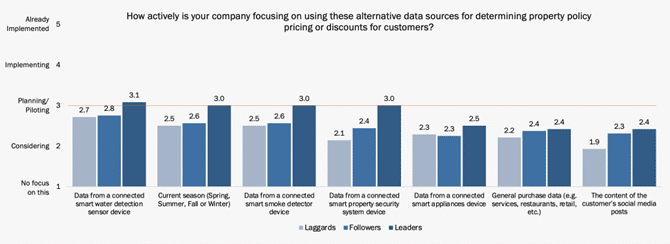

Leaders outpace the other segments in the use of new data sources for property pricing, but show less innovation compared to auto pricing data sources. (See Figure 7). With the growing gaps in coverage for customers due to financial challenges of rising property insurance rates, new and creative pricing options are crucial to help insurers close the protection gap by offering personalized coverage and pricing that may be more affordable.

Figure 7: Insurers’ activity levels in using new data sources for property insurance pricing

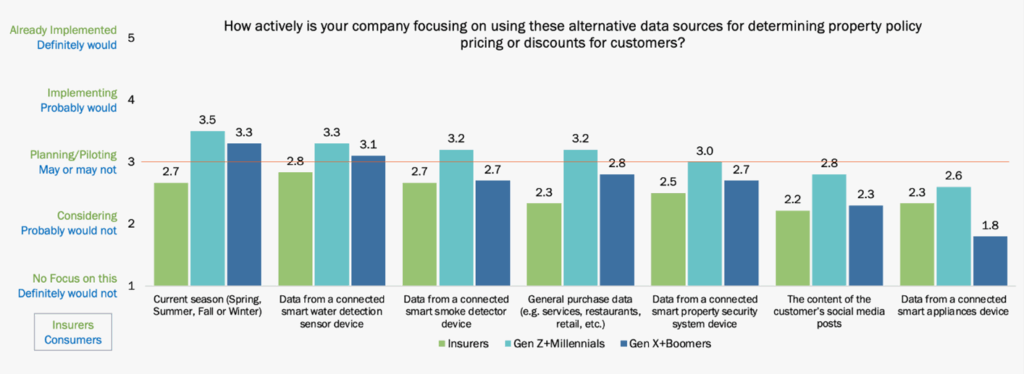

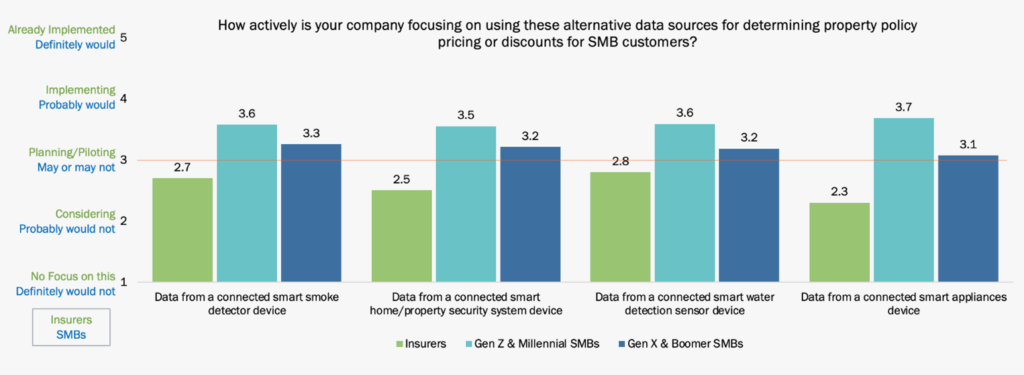

Our 2024 Consumer Research indicated homeowner and renter insurance with season-based rates were the most popular alternative pricing method. However, as seen in Figures 8 and 9, data from connected devices is equally popular with both consumers and SMBs (2025 SMB research), mirroring the acceptance of data from auto-connected devices.

Figure 8: Insurers’ activity levels compared to consumers’ perceptions on using new data sources for property insurance pricing

Figure 9: Insurers’ activity levels compared to SMBs’ perceptions on using new data sources for property insurance pricing

While we expect this interest from Gen Z & Millennials, the older generation’s acceptance is equally high, evidence of the rapid increase in use and acceptance of digital devices by all generations, highlighting the need for insurers to accelerate their use of connected and telematic devices for property.

L&AH Pricing

In the face of rapidly changing risk factors, it is increasingly crucial to have capabilities for evaluating individual risks, the exposure within an entire portfolio, risk appetite, and ultimately, profitability. In particular, supplemental health products have seen the need for more frequent pricing changes due to rising medical costs.

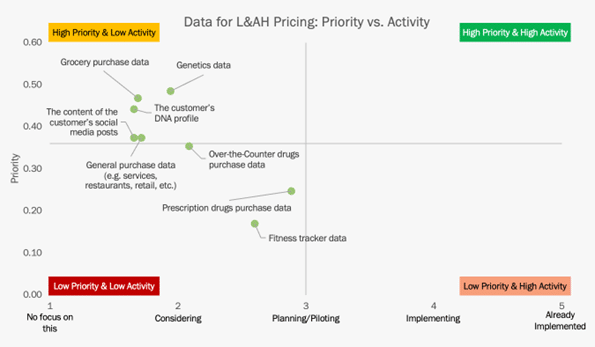

However, in contrast to P&C auto and property, adoption of new data sources for L&AH pricing is significantly lower, as shown in Figure 10. Prescription drug purchase data and fitness tracker data are the only two out of eight different data sources close to the Planning/Piloting phase, but they also have low priority. The other six data sources reflect high priority but are only near the Considering phase.

These diametric differences represent the struggle within the L&AH segment to clearly identify areas of priority to innovate pricing and rating for L&AH products. As P&C accelerates their focus on personalized pricing, L&AH will likely experience increased pressure and expectations to do the same. Piloting now is crucial to understanding the opportunity.

Figure 10: Insurers’ priority and activity levels in using new data sources for L&AH insurance pricing

When assessing progress based on Leaders, Followers and Laggards, Leaders clearly stand out across all data sources, but in particular, for using prescription and OTC drug purchase data as well as fitness tracker data, as shown in Figure 11. Despite their lead over Laggards and Followers across all categories, widespread adoption remains a challenge.

Figure 11: Insurers’ activity levels in using new data sources for L&AH insurance pricing

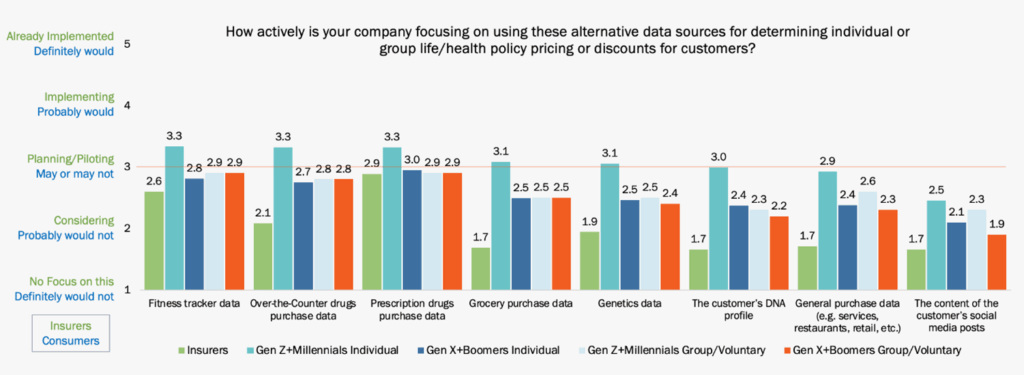

Our 2024 Consumer Research indicated an openness in using personal data sources to develop more accurate personal risk profiles for individual or group life/health policy pricing. In fact, customers are most willing to share data from fitness trackers and purchases of over-the-counter and prescription drugs to achieve this.

This customer expectation is completely opposite of what insurers are doing by very large margins, as shown in Figure 12. This large gap reflects a growing expectation gap that insurers must meet to acquire and retain business.

Figure 12: Insurers’ activity levels compared to consumers’ perceptions on using new data sources for L&AH insurance pricing

Pricing and Rating engines underpin data use for profitability

Data’s use across insurance verticals is growing at the perfect time. If customers are more interested in allowing data to be used than insurers are actively using it, that represents a field of opportunity. The next step in the process for insurers then becomes, “How do we prepare to use new sources of data?” Though there are undoubtedly a hundred answers to this question, two stand out.

- Audit current pricing and rating engines to determine their effectiveness in dealing with today’s and tomorrow’s data sources. Prepare to make quick course corrections and launch new products by making sure that pricing and rating engines are “intelligent.”

- Consider a holistic approach by P&C and L&AH segments to profitability that includes intelligent core transformation as another element of product development and pricing refinement. Intelligent core solutions that utilize AI, GenAI and Agentic AI, can ease pricing burdens by easing operational costs and streamlining all processes.

In any situation, it would be a wrong step to stand still at this moment in time and make no changes. In the same way, it would be a misstep to chip away at the insurance pricing issue with smaller projects aimed at incremental improvements that don’t account for AI’s ability to transform the whole enterprise and improve the whole insurance pricing equation.

The best step may be a simple conversation. Contact Majesco today to discuss any pricing constraints and challenges that are holding your teams back. Research Majesco Intelligent Core solutions for P&C and L&AH, Majesco Enterprise Rating for P&C and Majesco Intelligent Sales and Underwriting Workbench[DG1] to kickstart your efforts to price accurately. And check out Majesco’s recent innovations in AI-driven capabilities, insurance workflows, analytics and telematics that will prepare your organization to compete now and for years to come.

[i] Cox, Cynthia, ACA Insurers Are Raising Premiums by an Estimated 26%, but Most Enrollees Could See Sharper Increases in What They Pay, KFF QuickTakes, October 28, 2025

[ii] The Risk Right Now: Market Shifts Shaping U.S. Auto Insurance, 2025 LexisNexis® U.S. Auto Insurance Trends Report, LexisNexis, June 12, 2025

[iii] Sclafane, Susanne, “2025 Underwriting Profit and ‘Shop-a-Palooza’ Predicted for Auto Insurance,” Carrier Management, December 31, 2024, https://www.carriermanagement.com/features/2024/12/31/270001.htm?utm_content=shop-a-palooza-what-to-expect-for-personal-auto-insurance

[iv] Rice, Doyle, “’Sobering’ data shows US set record for natural disasters, climate catastrophes in 2023,” USA Today, September 11, 2023, https://www.usatoday.com/story/news/nation/2023/09/11/us-sets-record-weather-climate-disasters-2023/70822661007/