Blog

Insurance Analytics and AI Momentum Elevate Data to the Top of Insurer Priorities List

Agentic AI has a data problem.

Insurance Analytics and AI are a catalyst for a new era of intelligent insurance. Most insurers recognize this, but are stymied by a crucial hurdle: access to consistent, quality data.

The most lucrative benefits from AI will require data modernization that is difficult at best because many insurers yet operate on highly customized, legacy on-premise solutions that make it difficult to access data, let alone in real-time. For insurers to truly capitalize on AI, they will need cloud-native modern core solutions that provide access to all the operational data in real-time via a data lake, and the ability to extend with other third-party data in a unified data platform.

Data has always been the lifeblood of the insurance industry but today it is a vital asset in our digital world and increasingly crucial across every part of the insurance value chain. Its vitality is further elevated with GenAI and Agentic AI which are crucial to redefining the insurance operating model as an AI-powered core operations built around intelligence on tap, human–agent teams that enable insurers to scale rapidly, operate with agility and resiliency, and generate business value faster.

This new era of Intelligent insurance can’t do without them. The quandary is that data access is limited. From siloed data to limited access to core operational data, consolidation of data providers, and access at a price for some data, the industry has a significant gap between those with access to data and those without, resulting in competitive and market opportunity differences.

Neither business users nor intelligent systems have adequate access to data—and in truth—they may not even be on target to use the right data. Without unified, reliable, real-time access to operational data as well as the ability to easily and reliably ingest unstructured data, insurers cannot fully leverage AI to redefine the insurance business across underwriting, policy, billing, claims, and customer experience at scale.

Data modernization is now an AI imperative, but data modernization has been used to describe several things. So, it really needs a simple definition.

What is data modernization in insurance?

In short, data modernization in insurance entails both:

- a data platform that provides real-time access to operational data across the enterprise and

- employing intelligent systems that use that data with AI, whether in ML models or within business processes using GenAI or Agentic AI.

Where are insurers right now in their quest for data modernization in insurance?

Majesco’s thought-leadership report, Strategic Priorities 2026: A New Era of Innovation and Disruption Offers Real Business Value covers a broad spectrum of insurer tech priorities. In a section devoted to Data & Analytics Priorities, Majesco sheds light on insurers’ states of mind as well as their willingness to transform their data frameworks in order to meet AI demands. We also look at transformation momentum — how quickly are insurers implementing individual data & analytics capabilities? Which ones seem to take priority?

What is the hurdle for insurers?

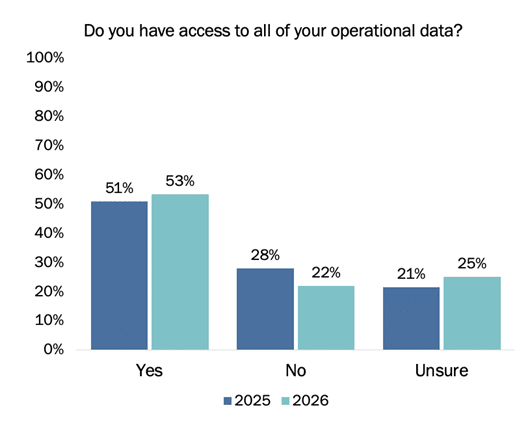

The business demand for unified, modernized data is logical. Every aspect of the insurance business uses data. With Advanced Data & Analytics as a top strategic priority from our Strategic Priorities 2026 Research, it is concerning that only 53% of insurers claim to have access to all of their operational data, according to the Majesco report. (See Fig. 1)

The hurdle to accessing this operational data—a foundational requirement for AI, automation, analytics, and modern operating models—is impeded by the heavy legacy core system environment most insurers operate within.

Given the industry’s growing emphasis on intelligence-driven operations, the lack of progress to a native-cloud core solution is a consequential finding.

Figure 1: Year-Over-Year Changes in Reported Access to All Operational Data

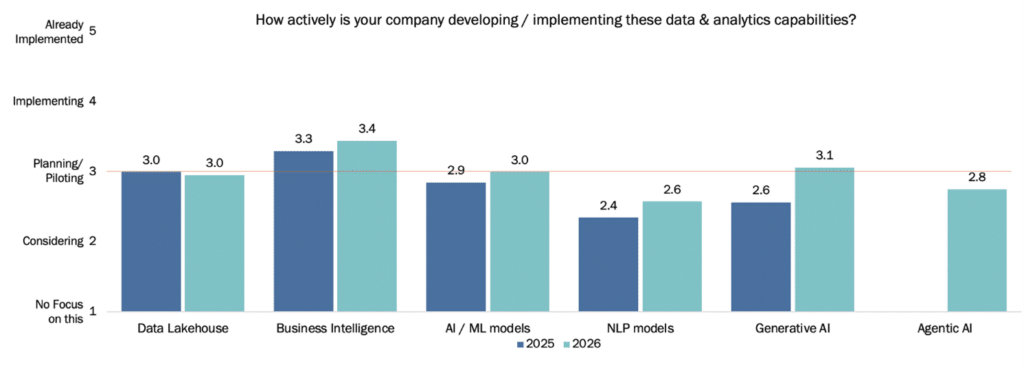

The Majesco research found that year-over-year results demonstrate clear upward momentum in a range of data and analytics capabilities. (Figure 2) Business intelligence, AI/ML models, and NLP models each rose modestly, hovering around Planning/Piloting. The strongest gains are in Generative AI capabilities, growing 19%, and Agentic AI, new in this year’s survey, reaching the Planning/Piloting phase at a rapid pace.

Despite these gains, the overall activity levels remain moderate, indicating that while insurers are moving toward intelligence-driven operations, they are likely limited due to legacy systems that inhibit enterprise-wide AI adoption.

Figure 2: Year-Over-Year Changes in Developing / Implementing Data & Analytics Capabilities

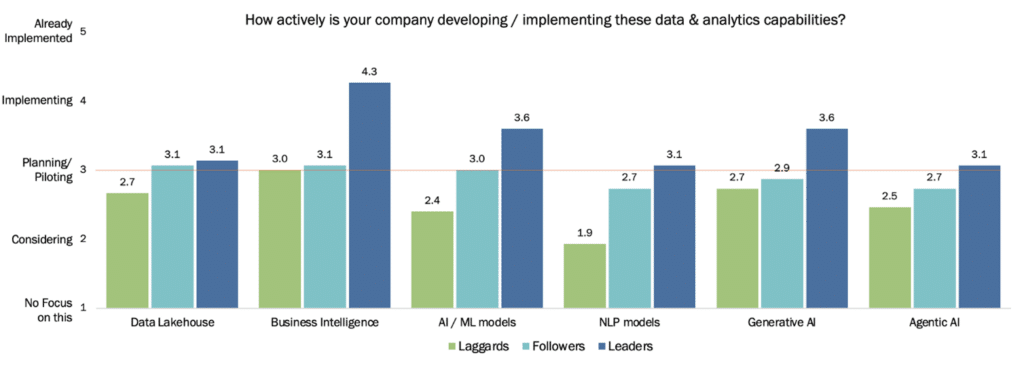

As seen in Figure 3, Leaders reflect the highest maturity across all categories. They show strong activity in Business Intelligence (4.3), AI/ML model development (3.6), and Generative AI (3.6), all at or near the Implementing phase — and not getting hung up in the experimental phase. NLP models and Agentic AI are both at the Planning/Piloting level, but we would expect these to dramatically accelerate in next year’s survey.

Followers cluster in the Planning/Piloting phase—active enough to demonstrate intent but not progressing at the scale or velocity necessary to close the gap with Leaders. Laggards are even slower across the board, just at or below the Planning/Piloting phase, signaling early-stage experimentation rather than meaningful adoption that creates an even larger gap to Leaders.

We expect this gap to widen until Followers and Laggards replace legacy core systems with cloud- and AI-native core. Until then, they will remain at an increasing disadvantage.

Figure 3: Development / Implementation of Data & Analytics Capabilities by Leaders, Followers, and Laggards

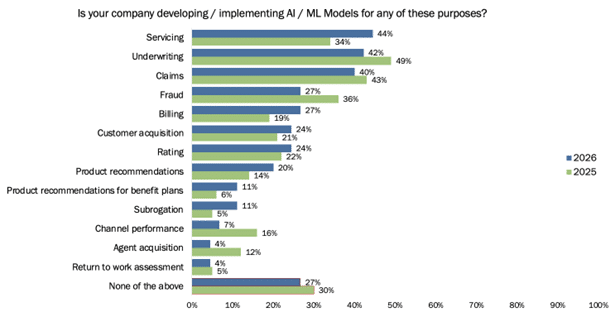

Insurance use cases for AI/ML models show off functional priorities.

In a deeper dive into AI/ML model focus, the year-over-year comparison of use cases seen in Figure 4 reveals a significant realignment in insurers’ priorities. Underwriting, while still one of the top use cases, declines seven percentage points, signaling a shift in AI focus from traditional target areas like underwriting augmentation toward more operationally-oriented applications. Claims-related AI usage drops 3 points, and fraud drops significantly by 9 points, highlighting the same shift to operations focus.

Interestingly, billing increases by 8 percentage points and servicing accelerates substantially by 10 points, reinforcing the industry’s shift toward AI-assisted workflow automation across the service areas for customers.

Conversely, more strategic or growth-oriented use cases, such as channel performance and agent acquisition, dropped by 9 and 8 percentage points, respectively.

Figure 4: Year-Over-Year Changes in Developing / Implementing AI / ML Models

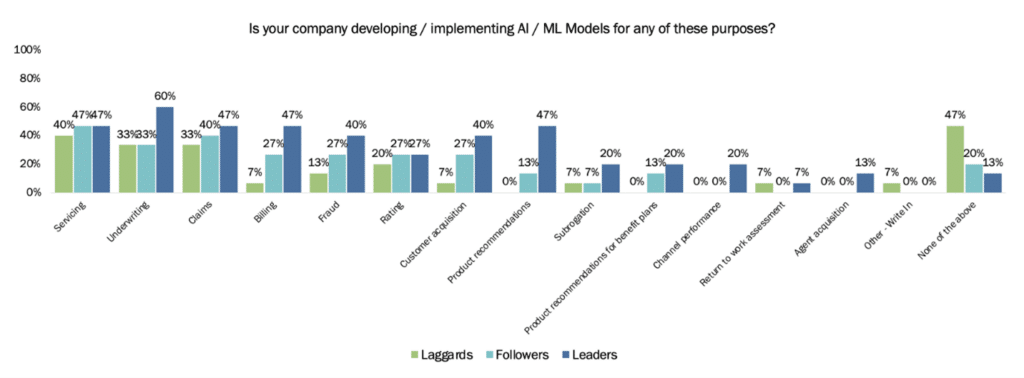

Leaders demonstrate the broadest adoption and the deepest use across nearly all categories of AI/ML model development, as seen in Figure 5. High-impact areas like underwriting and claims show Leaders’ adoption levels of 47–60%, and similar strong engagement in fraud, servicing, and billing.

Leaders also exhibit materially higher adoption in growth-oriented use cases, such as customer acquisition (40%) and product recommendations (47%), areas where Followers and Laggards show much lower activity.

Followers’ moderate adoption on nearly half of the use cases (often in the 27–40% range) suggests they may be in the early stages of building a meaningful AI foundation but have not yet achieved the scale, consistency, or breadth of Leaders.

While Laggards’ strongest categories are servicing, underwriting, and claims, their extremely low AI adoption across nearly every other category, underscores their limited readiness for intelligence-driven operations that is placing them well behind Leaders and Followers, creating a significant disadvantage for them

Figure 5: Development / Implementation of AI / ML models by Leaders, Followers, and Laggards

What are the use cases for Agentic AI in insurance?

AI is reshaping the way companies organize work and manage talent. GenAI is changing the way we ask and answer questions and can now be set up to act on its own to reach specific goals. Agentic AI agents are addressing the complexity of tasks that will change the operating model and cost structure of organizations. Agentic AI is rapidly moving beyond automation with AI agents operating in concert with humans embedded into workflows. Agentic AI insurance use cases must be supported by a redesigned operating model, governance structure, organizational structure, and talent base.

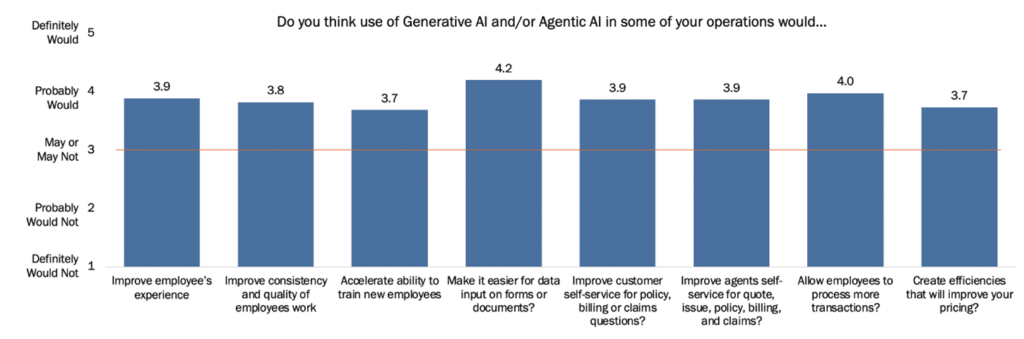

In the 2026 report, Majesco took a deeper dive into both GenAI and Agentic AI insurance use cases given the excitement and perceived pace of adoption in the industry. The perceived impact of Generative AI and Agentic AI across insurance operations is broadly positive, with every item scoring well above the midpoint of the scale. This reflects clear evidence that insurers believe AI will meaningfully enhance operational performance and customer-facing interactions—both top-of-mind issues and priorities.

The strongest benefit is eliminating manual data input (4.2) as seen in Figure 6, reflecting widespread recognition that AI can dramatically reduce manual effort in completing forms, interpreting documents, and handling unstructured information by ingesting and populating the data automatically.

Expectations that AI will improve employee productivity and enable more throughput also scored high (4.0), signaling confidence that automation and intelligent workflow orchestration will increase scalability and reduce cycle times which will drive lower costs and improve expense ratios.. Value for customer and agent self-service—both scoring 3.9—underscores AI’s potential to reduce friction, simplify inquiries, and elevate digital interactions across policy, billing, and claims.

Equally high, employee experience (3.9), work quality and consistency (3.8), and accelerating employee training (3.7) reinforce a broader business process value beyond throughput by helping to support positive experiences and enforce business compliance. Insurers see AI not only as an operational tool but as a workforce enabler that augments decision-making and reduces repetitive tasks. More importantly, it strengthens the organization’s talent model, compliance, and analytical rigor.

This aligns with Microsoft’s Work Trend Index 2025 research, on the concept of the Frontier Firm defines it as a company powered by intelligence on tap, run by human-agent teams, and defined by a new role for every employee: the agent boss. For insurance specifically, this means the top five to ten percent of organizations that dramatically outperform their peers — not by working harder, but by fundamentally redesigning how humans and intelligent systems work together.

Collectively, these results reinforce the broad industry view that GenAI and Agentic AI are the catalysts for broad-based improvements across the value chain, with the most immediate gains expected in productivity, efficiency, data handling, quality, consistency, and self-service capabilities.

Figure 6: Expected impact of GenAI / Agentic AI on operations

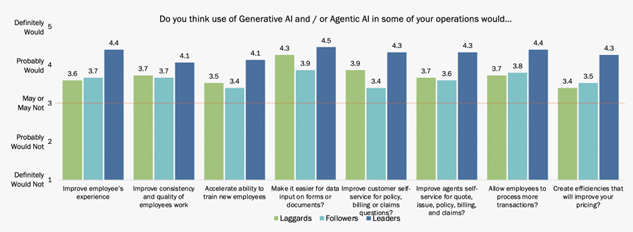

Not surprisingly, Leaders are significantly more optimistic about AI’s benefits, with consistent scores between the “Probably would” and “Definitely would” stages. Encouragingly, Followers and Laggards show similar ratings of moderate optimism, with Laggards actually ahead of Followers on data input on forms and customer self-service.

These differences reflect more than sentiment; they reflect readiness.

Leaders believe AI will transform operations because they have already invested heavily in core systems transformation to the cloud and have strong AI foundations. Followers and Laggards are cautiously optimistic but still constrained by inconsistent data maturity and legacy systems.

Given the pace of adoption, Followers and Laggards are significantly at risk of falling so far behind that it will be extremely difficult or too expensive to catch up.

Figure 7: Expected Impact of GenAI / Agentic AI on Operations by Leaders, Followers, and Laggards

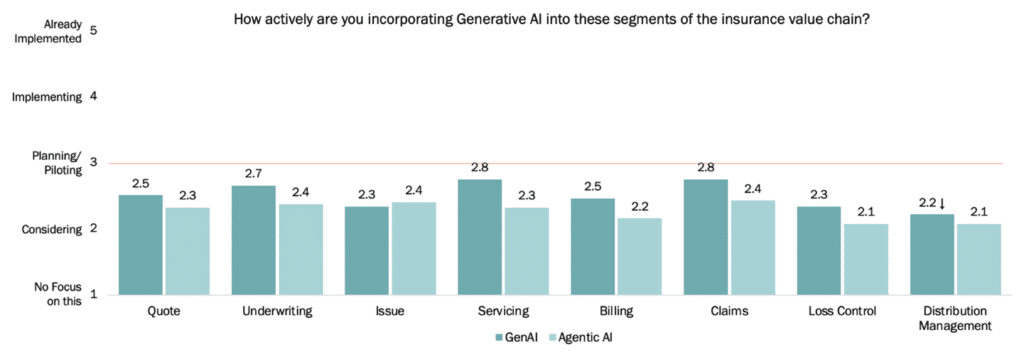

Across every part of the insurance value chain, GenAI currently outpaces Agentic AI in adoption, revealing an early but meaningful maturity gradient as insurers move from assistive to autonomous intelligence, as seen in Figure 8. Activity levels for GenAI run approximately 0.2–0.5 points higher than Agentic AI, with the widest gaps appearing in underwriting, servicing, and claims—areas where the stakes of automation are high, and insurers remain cautious about introducing autonomous, multi-step decision-making.

This pattern reflects a natural progression: GenAI is being deployed first to accelerate documentation, summarization, and data-handling tasks, while Agentic AI trails as organizations work to build the governance, staff capabilities, data integrity, and workflow redesign needed to support autonomous orchestration. In lower-risk, more structured domains such as billing, distribution management, and loss control, the gap narrows, signaling where Agentic AI is likely to take hold earliest.

Together, these differences highlight a sequential adoption path in which insurers use GenAI to strengthen operational foundations before moving into the more transformative, end-to-end automation enabled by Agentic AI. This progression will ultimately separate the insurers prepared for the Intelligent Insurance Era from those still navigating the fundamentals.

Figure 8: Levels of activity in incorporating Generative AI / Agentic AI into the insurance value chain

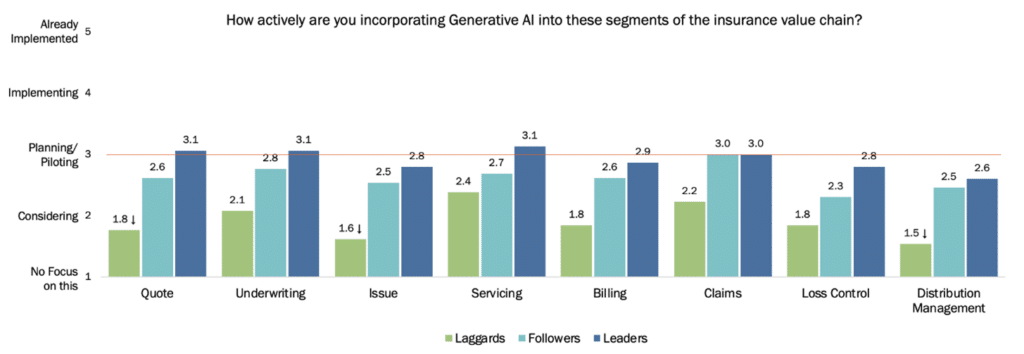

Leaders score GenAI markedly higher across the entire value chain, as seen in Figure 9, hovering around the Planning/Piloting phase across all segments. Encouragingly, Followers maintain moderate engagement, just slightly lower than Leaders, demonstrating strong interest but less maturity.

However, Laggards trail significantly, with activity levels around the Considering phase, indicating minimal or experimental use at best—creating a significant strategic and operational risk for their organizations.

Figure 9: Levels of activity in incorporating Generative AI into the insurance value chain by Leaders, Followers, and Laggards

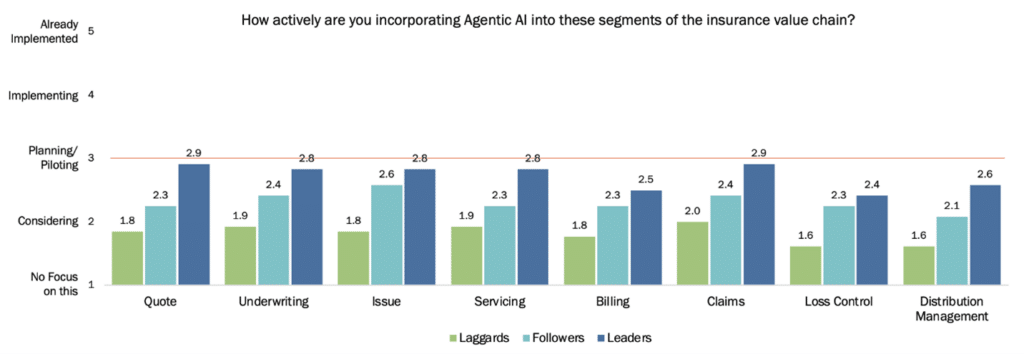

Where Agentic AI is Taking Hold in Insurance

Similar to GenAI, Leaders are materially more focused on Agentic AI activity across all value chain segments, as seen in Figure 10, albeit not as high, given the relative newness of Agentic AI. Leaders score highest in underwriting (2.8), servicing (2.8), quote (2.9). issue (2.8), and claims (2.9), indicating early investment in agentic workflows capable of autonomous orchestration, proactive task execution, and multi-step reasoning. Followers sit in the middle, just above the Considering phase, while Laggards remain at or just below this level, once again creating risk for their organizations due to the lack of focus.

Figure 10: Levels of activity in incorporating Agentic AI into the insurance value chain by Leaders, Followers, and Laggards

To truly capture the business value of AI, insurers must invest in a new technology foundation underpinned by native-cloud and AI core system, as well as workforce upskilling, with its new roles, workflows, and mindsets, and change management to embrace the new operating model. Insurers that strengthen both their AI capabilities and human-centric approach across the business operating model will attain a true competitive edge.

Unified data deserves a unified approach

If the Majesco 2026 Strategic Priorities report indicates one thing conclusively, it is that the future of AI in insurance is an enterprise-wide future. The application of data won’t abide a one-source and one-application approach. Data strategies will need to be holistic. Cloud and AI-native core solutions are crucial.

Insurers need a strategy and then execute it rather than experimenting with AI.

The Leaders pulling ahead are not asking ‘Where can we try AI?’ They are asking ‘Where can we not use AI?’ They are redesigning their entire operating model around intelligence. Inaction is not a neutral position. It is a strategic choice with real business consequences. And 2026 is the year that choice becomes irreversible. This brings us to the core challenge facing every insurer today.

Majesco is aligned to this vision of intelligent insurance business. But what we do differently is provide the intelligent solutions that provide the foundation and path to this future with access to all their data in a data lakehouse, access to embedded analytics including BI, GenAI with Majesco Copilot, and an array of Agentic AI agents as part of the core, not add-ons. It is why we are recognized as the AI leaders for both P&C and L&AH core. Our new Spring 26 product release brings more to our customers to continue this transformation.

Find out how your organization can redefine your future in a new era of intelligent insurance. Contact Majesco today. And, for more answers on what it will mean to be an AI-powered intelligent insurer, be sure to watch Majesco’s latest webinar, The Frontier Insurer: Powered by an AI Intelligent Foundation and New Operating Model.